Interval estimation

Lecture 22

2026-04-13

Also

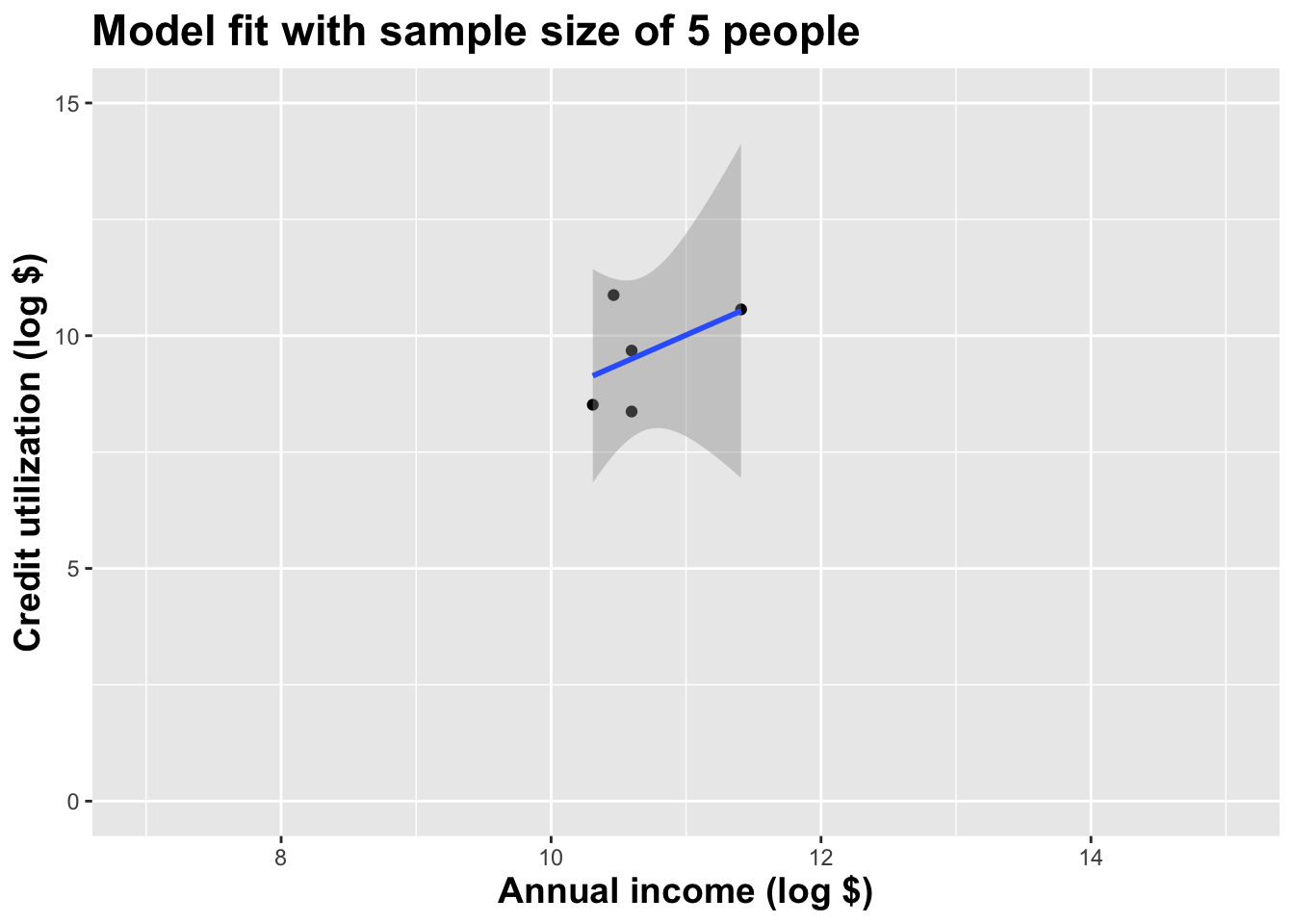

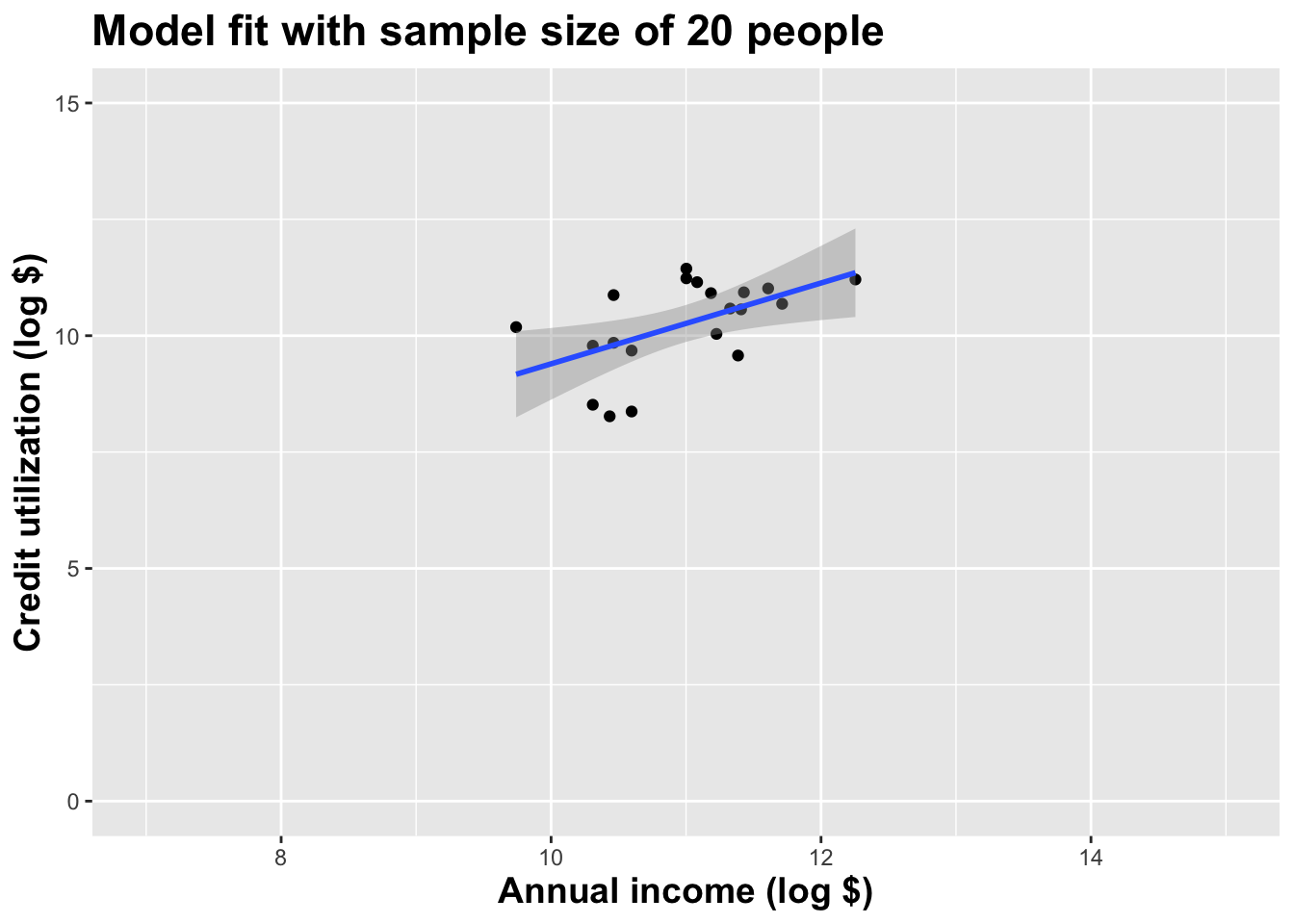

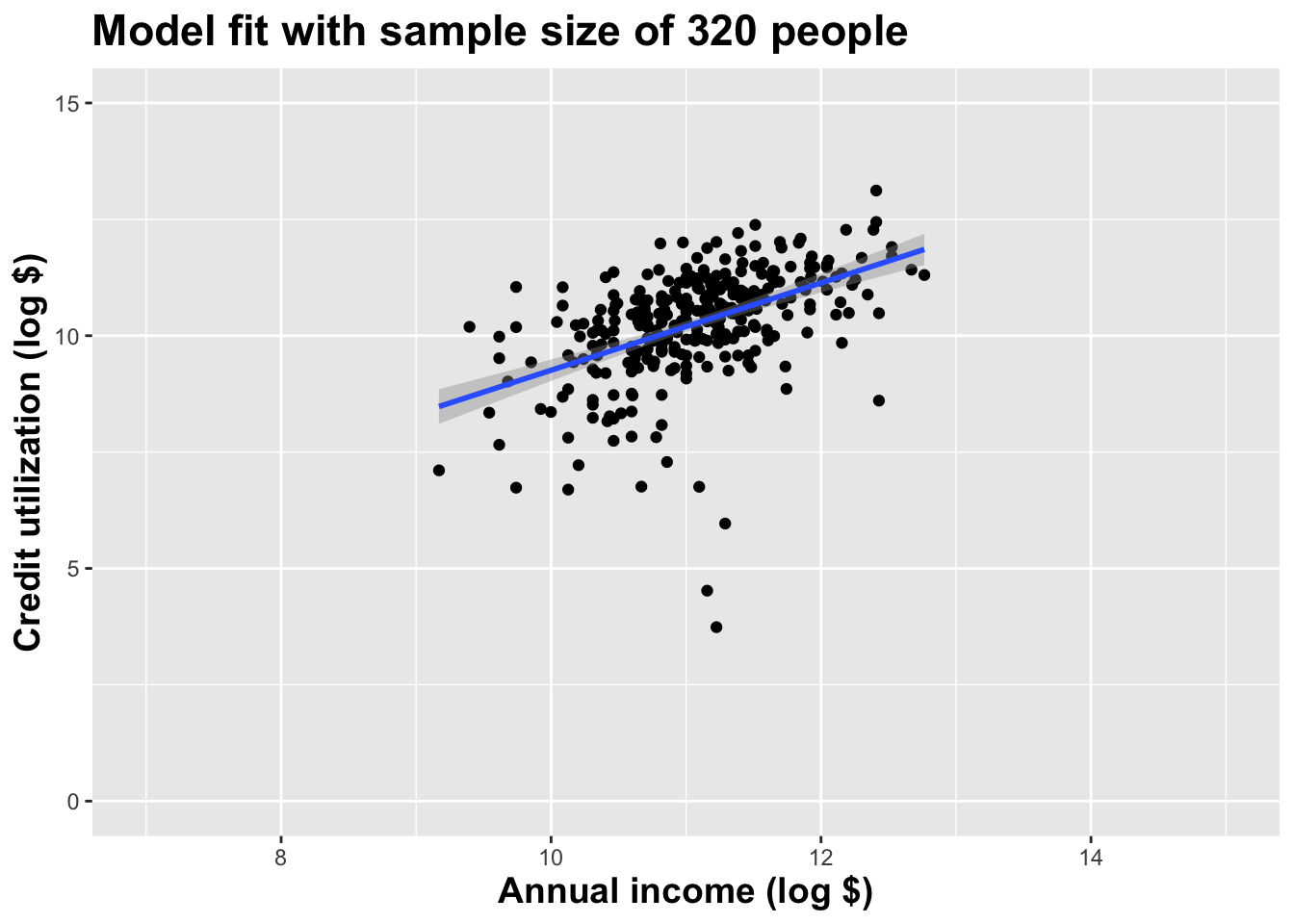

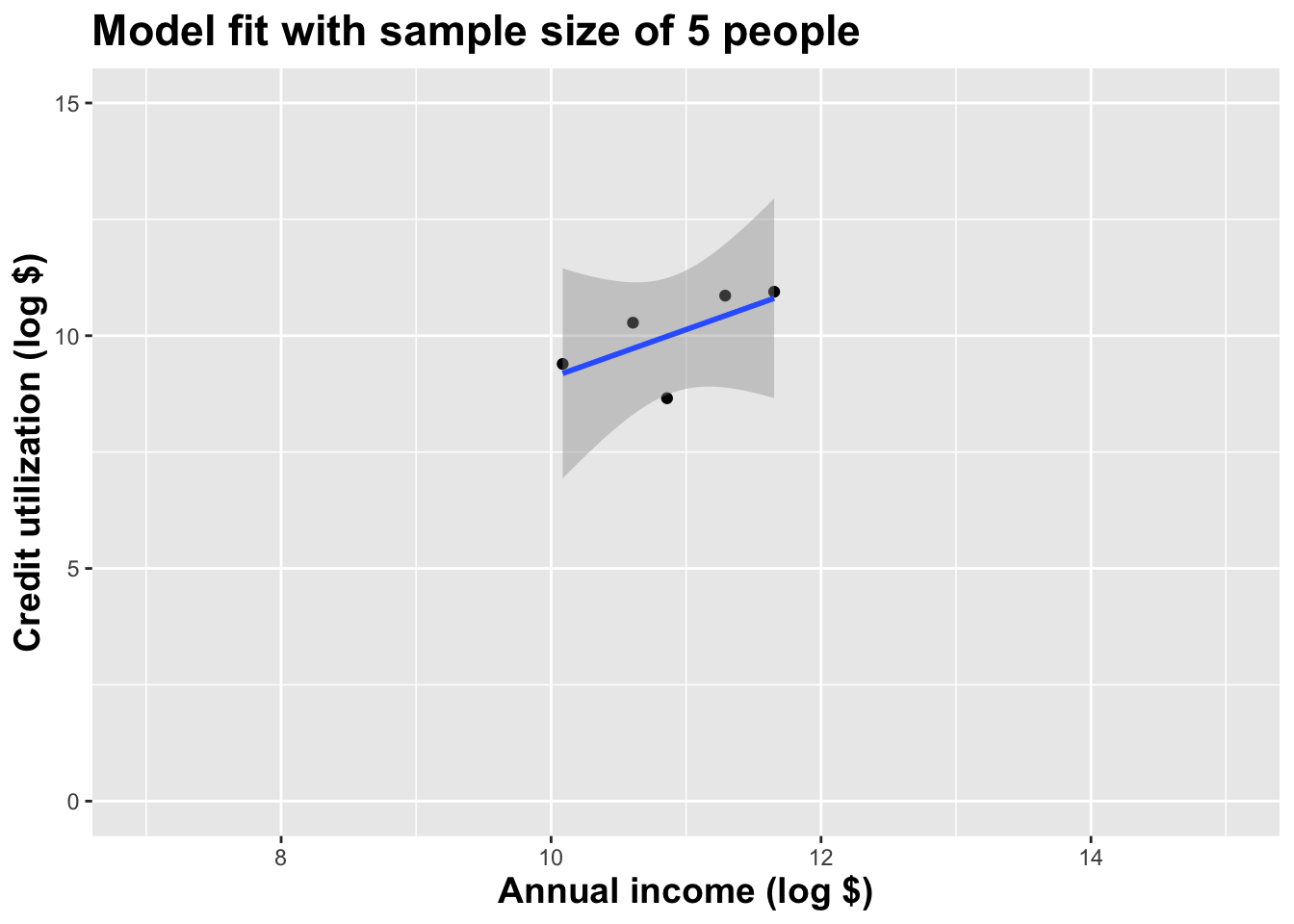

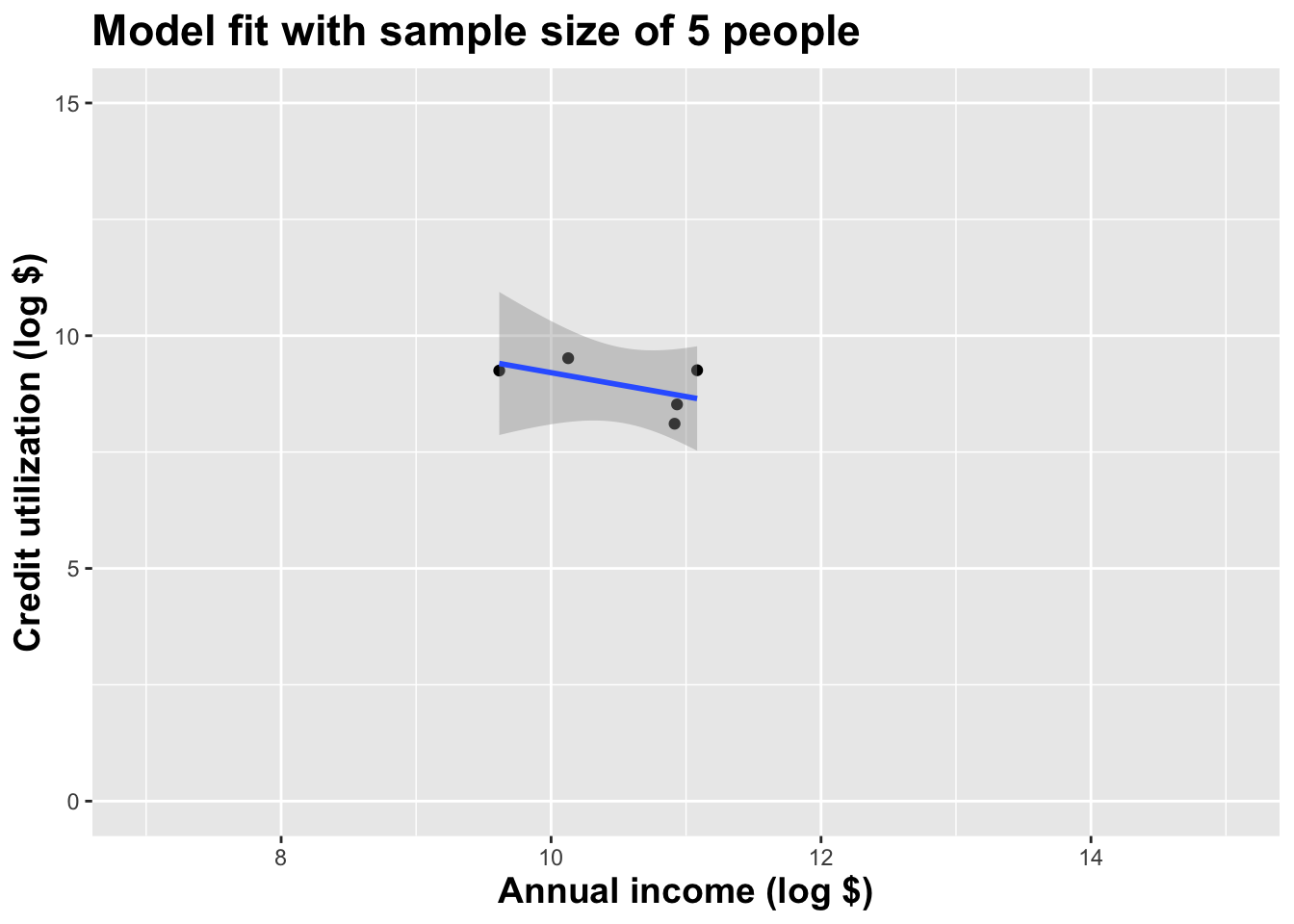

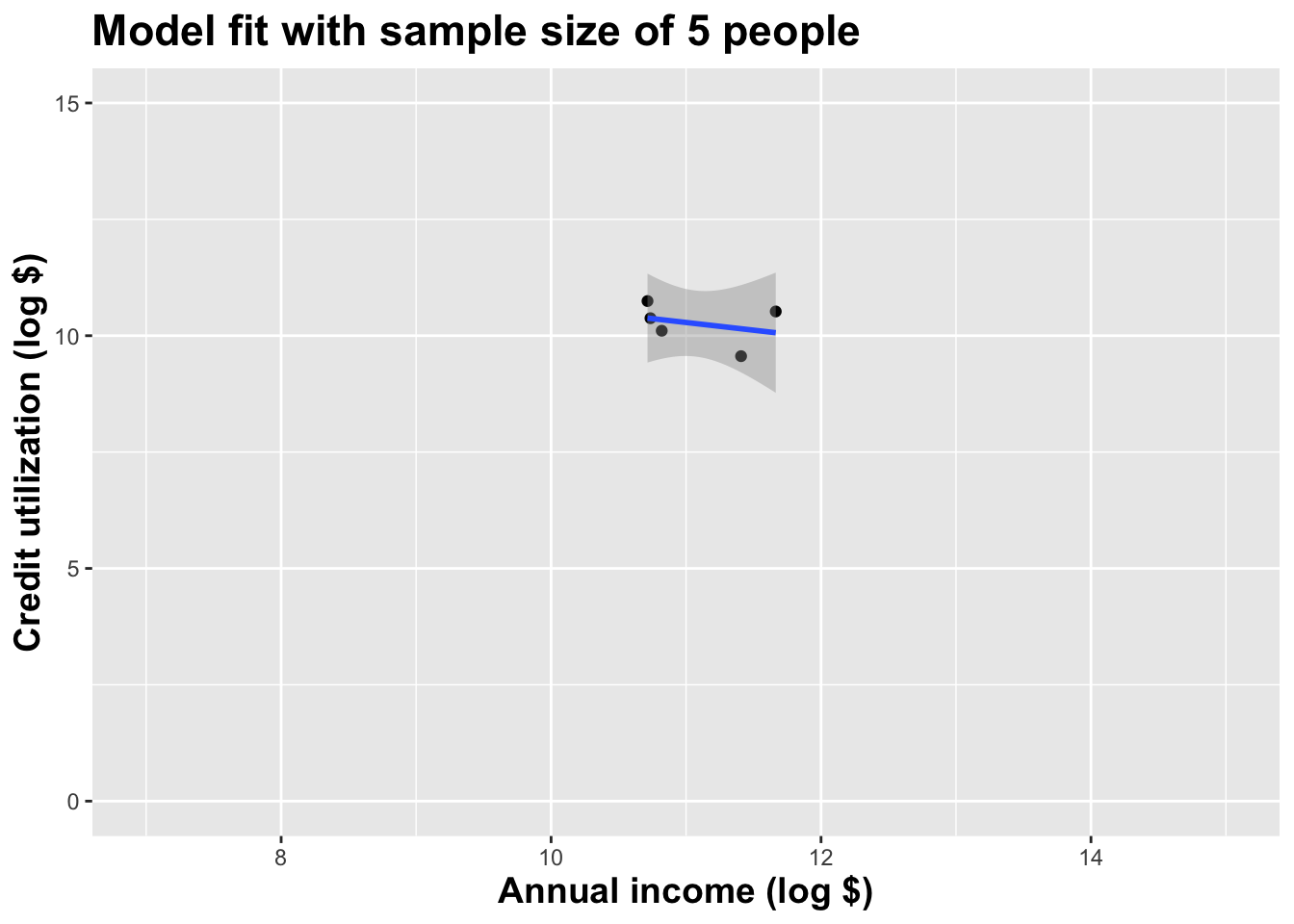

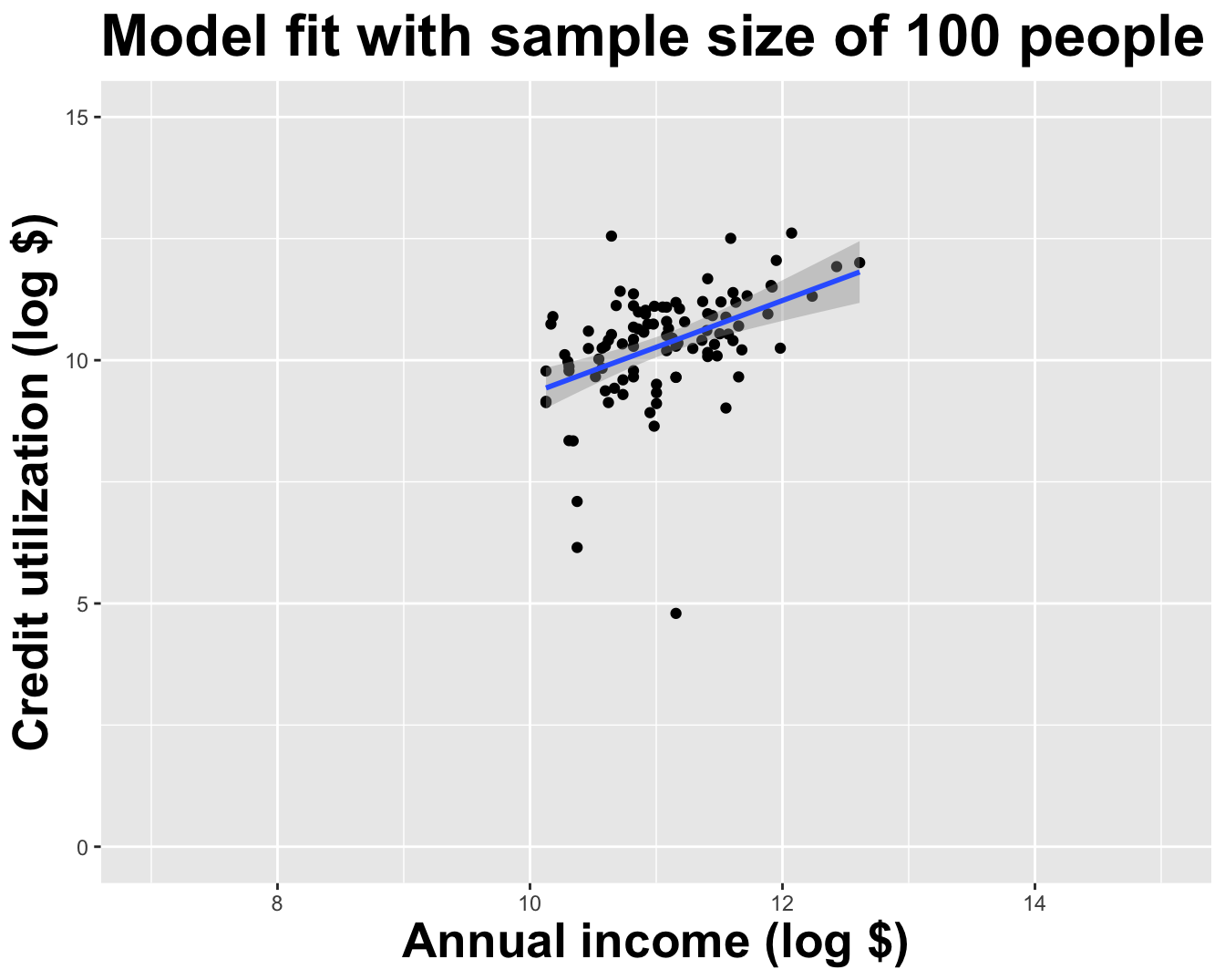

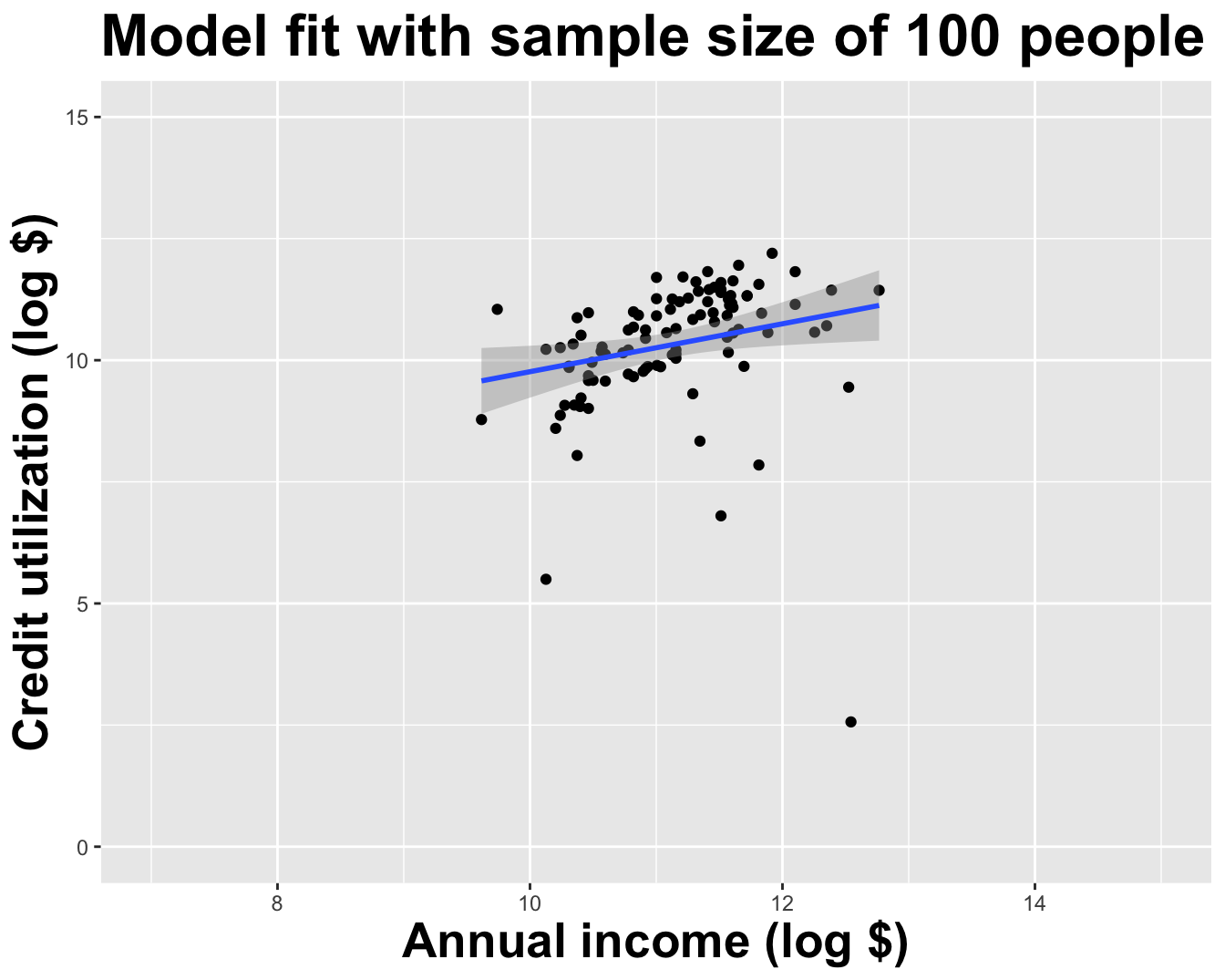

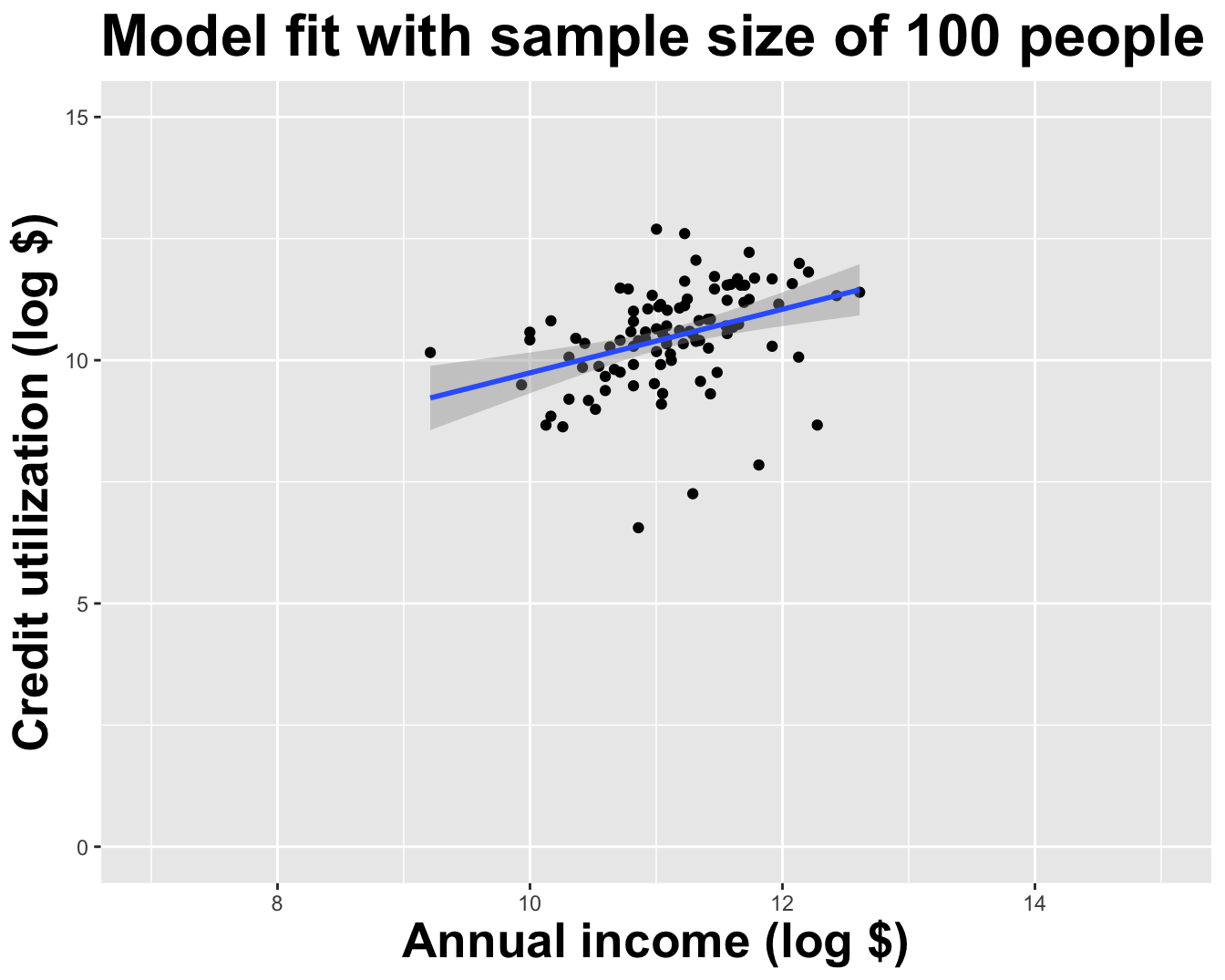

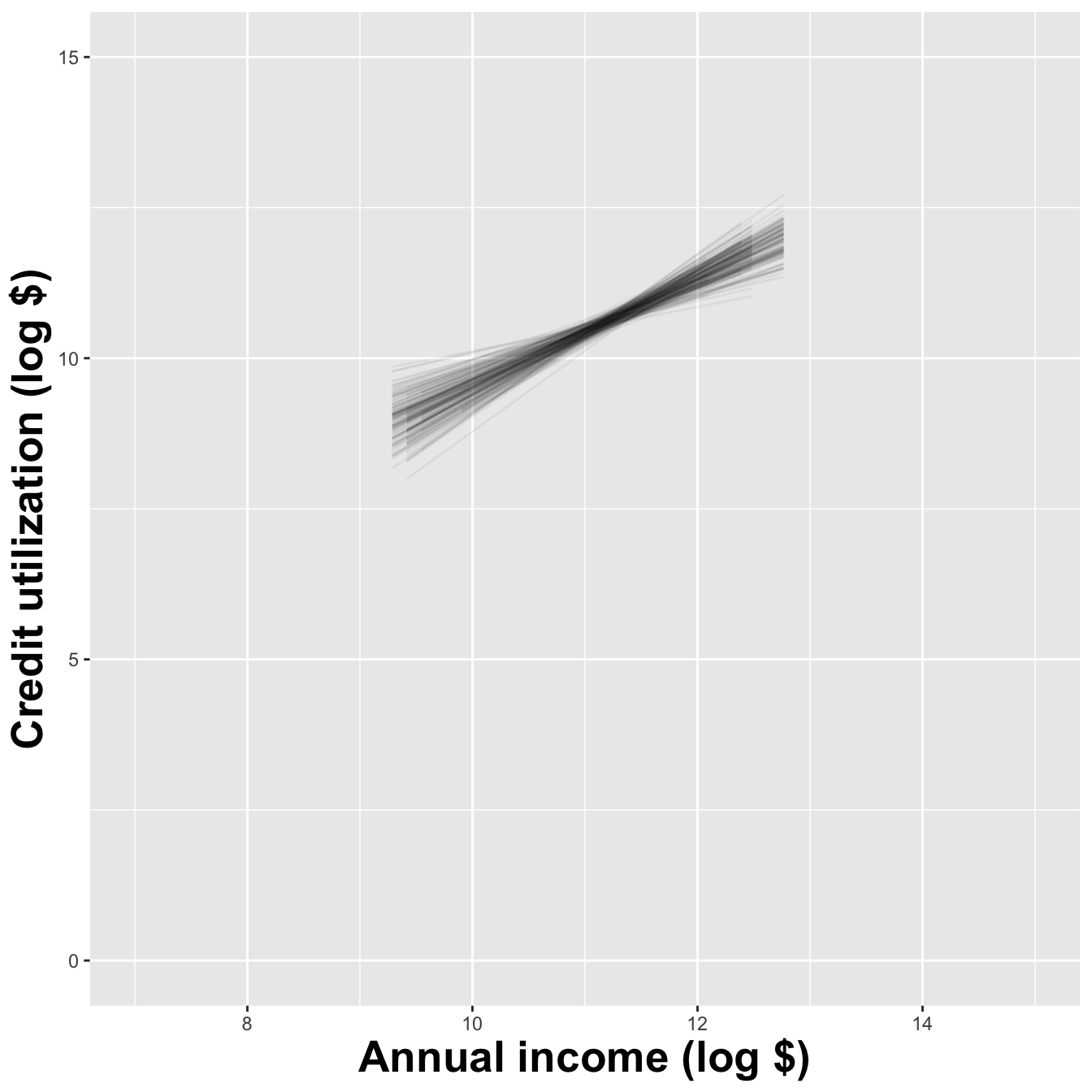

Model fit with five observations

(I just took logs to make the picture prettier.)

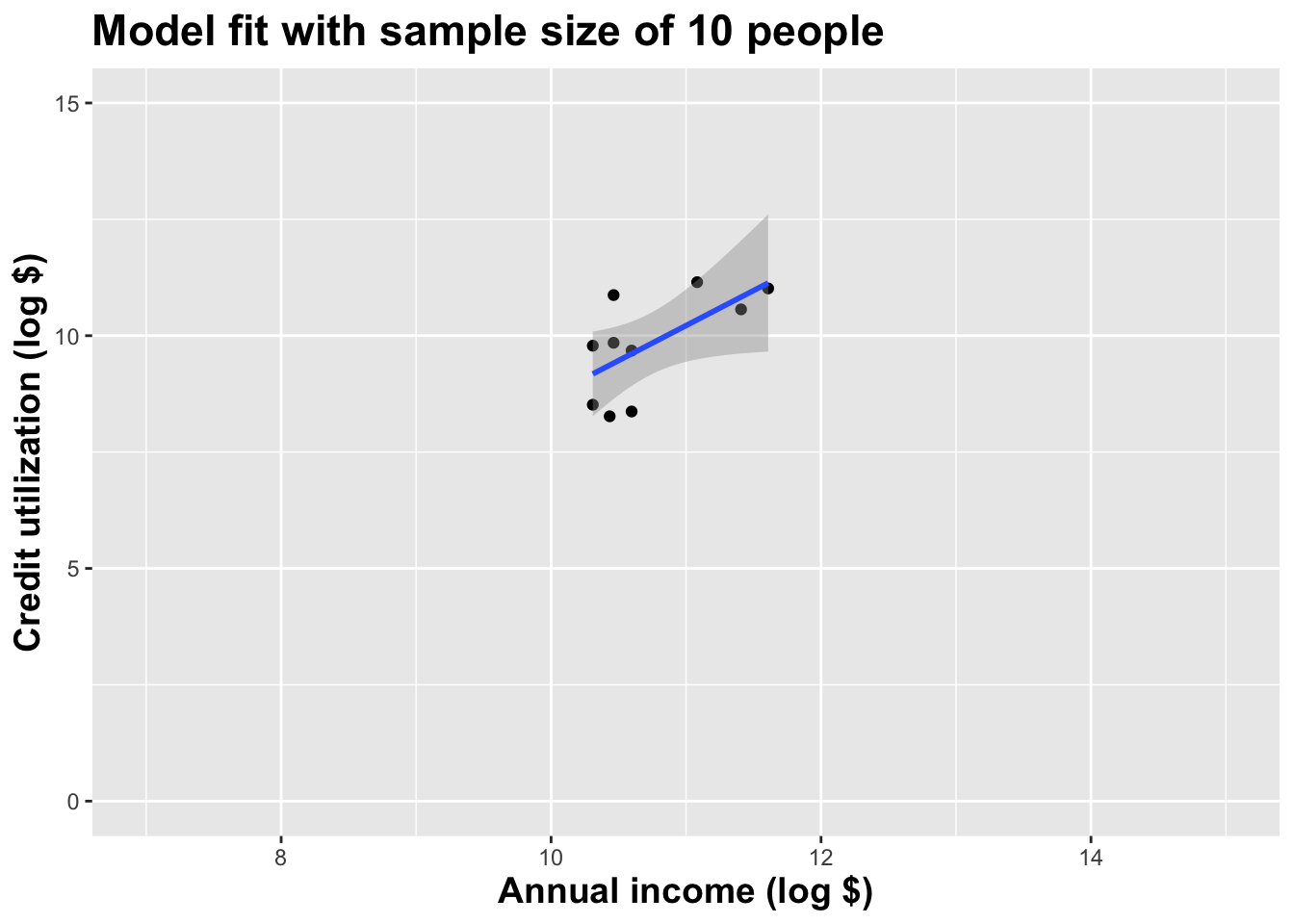

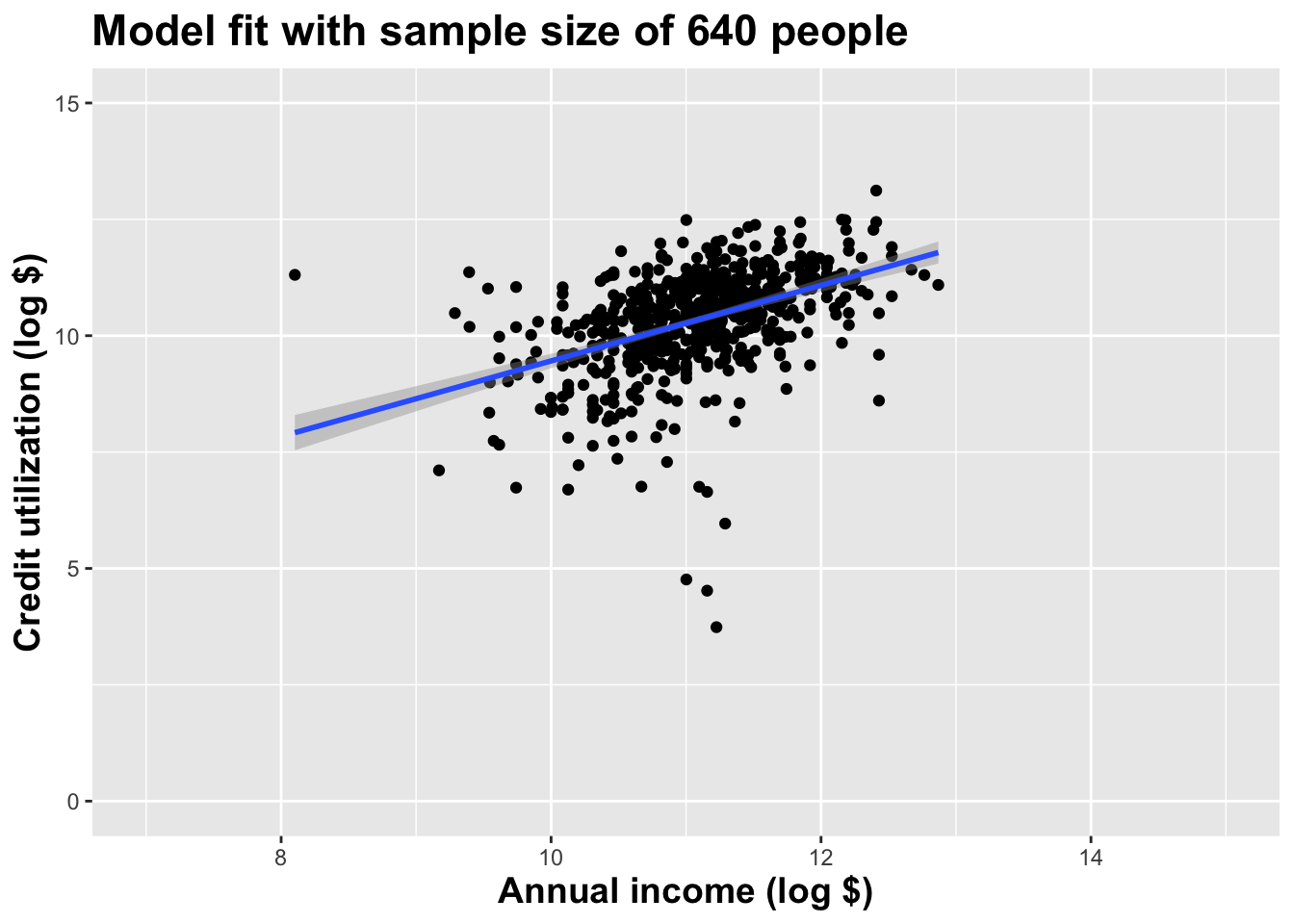

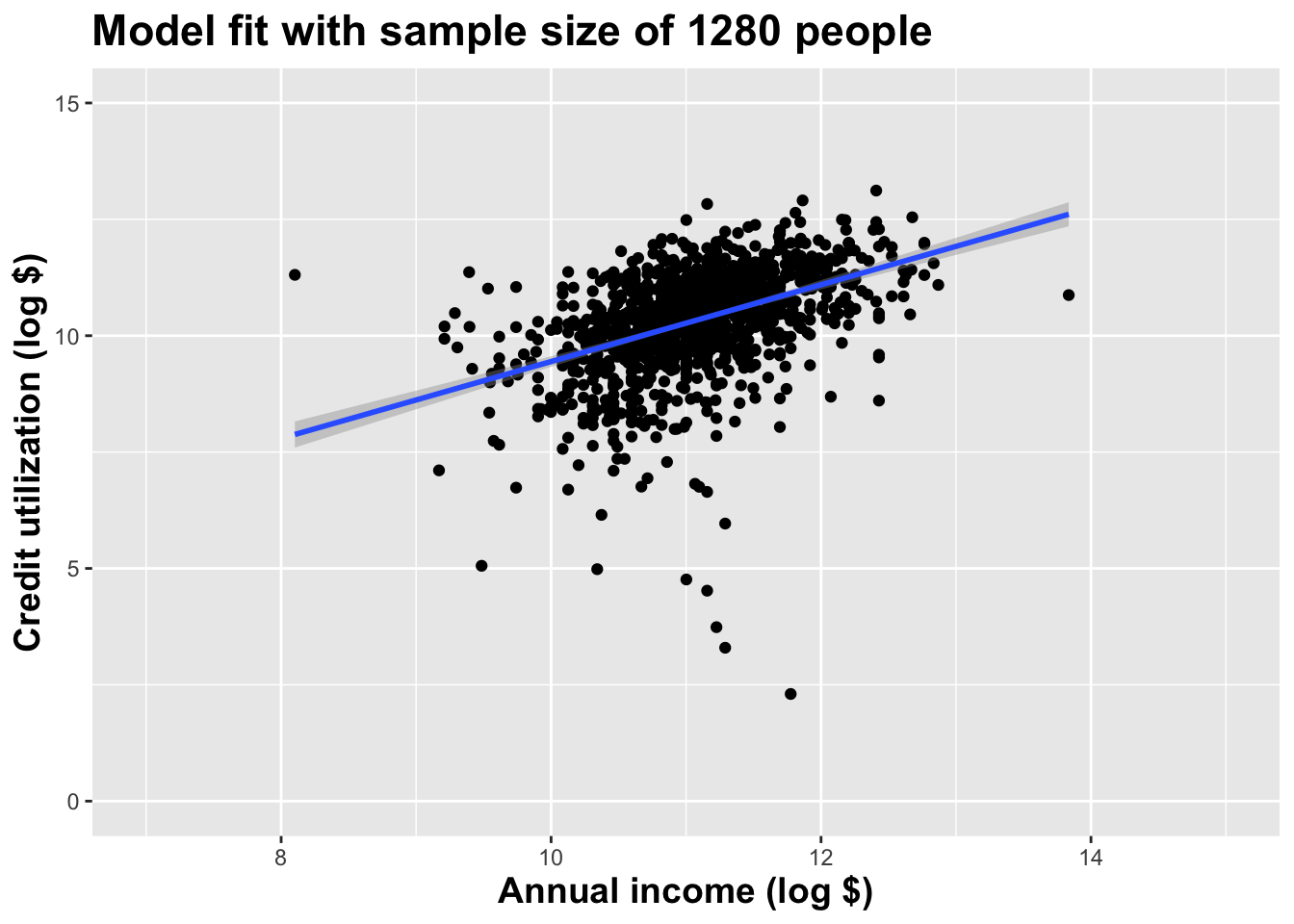

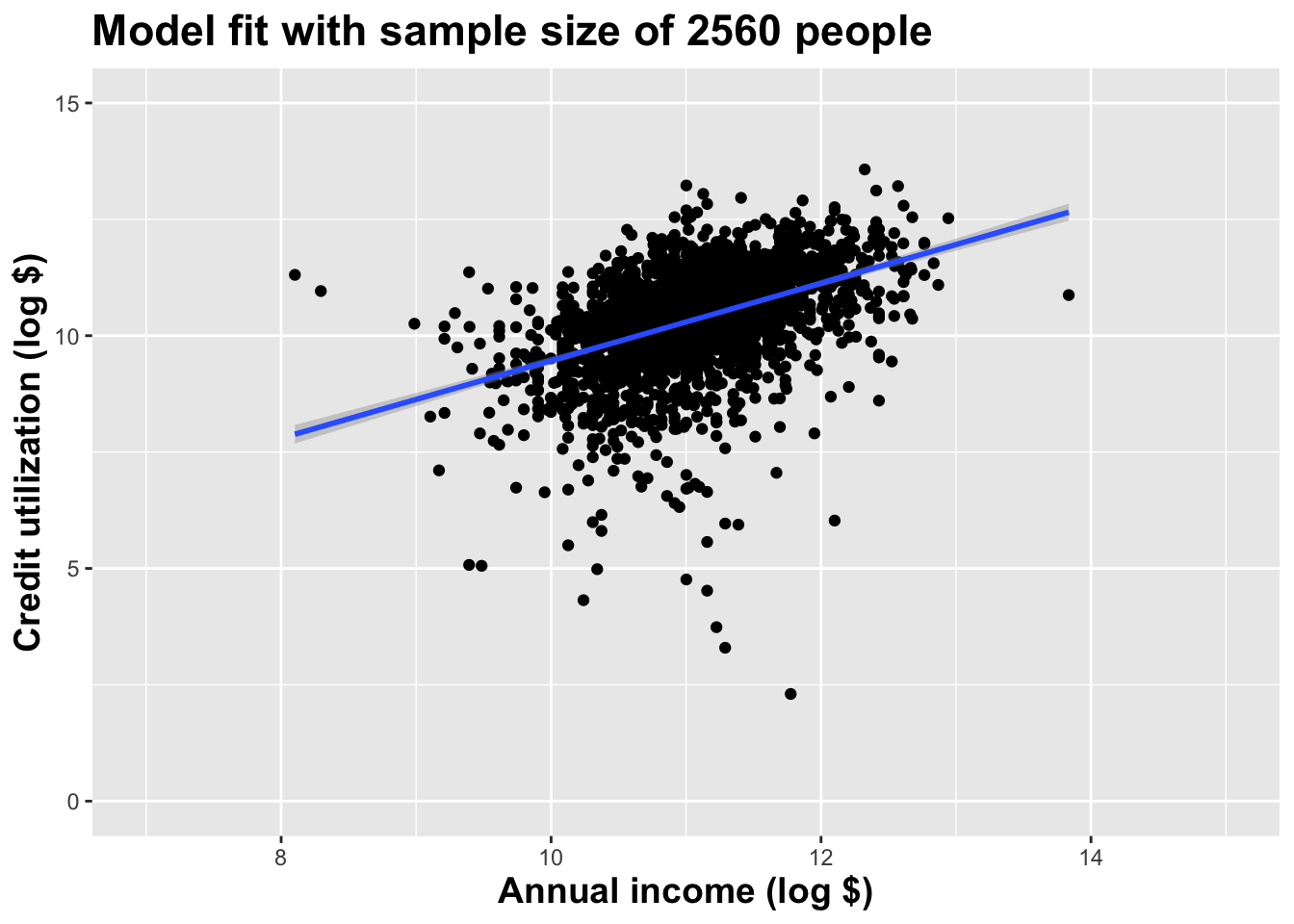

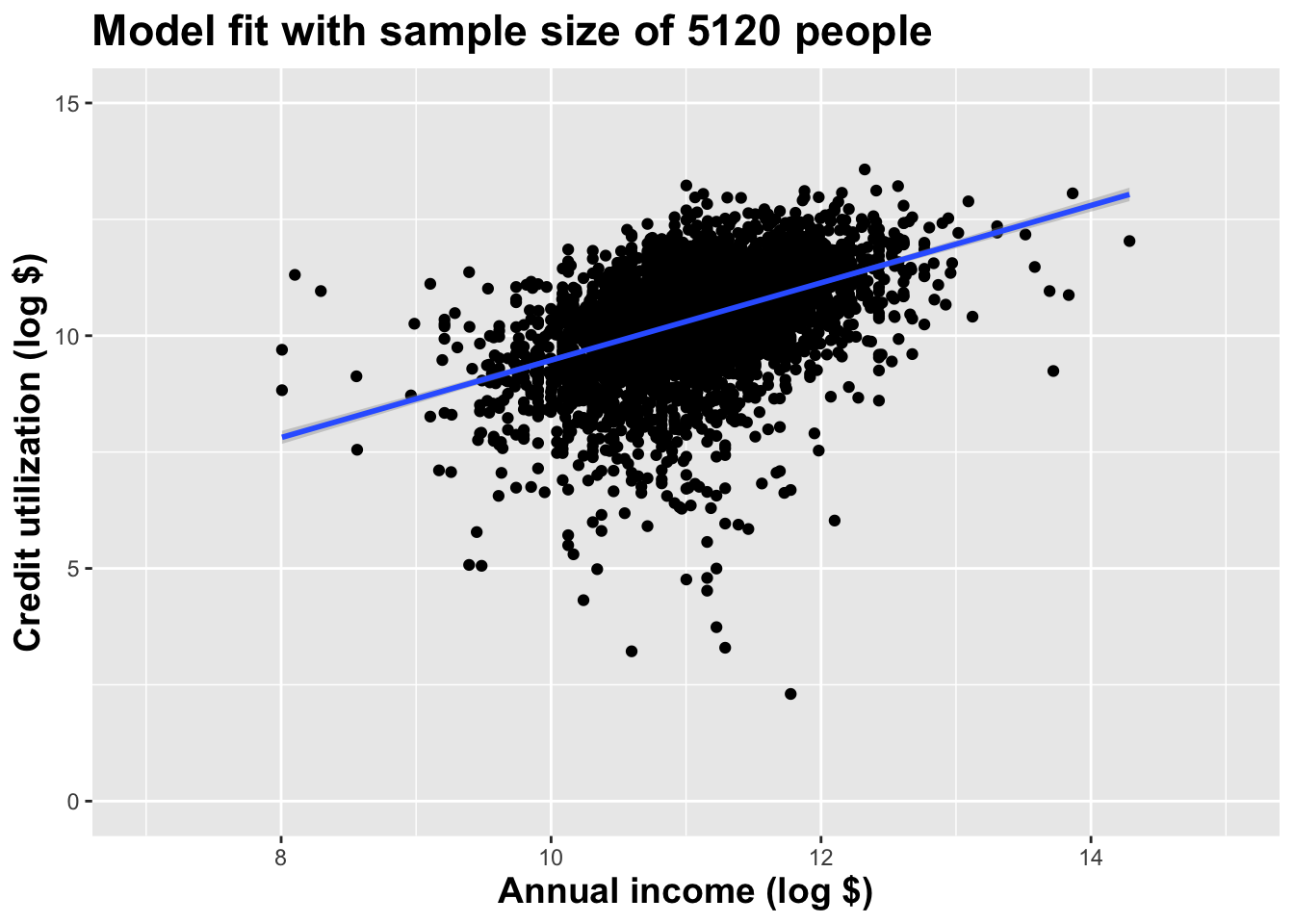

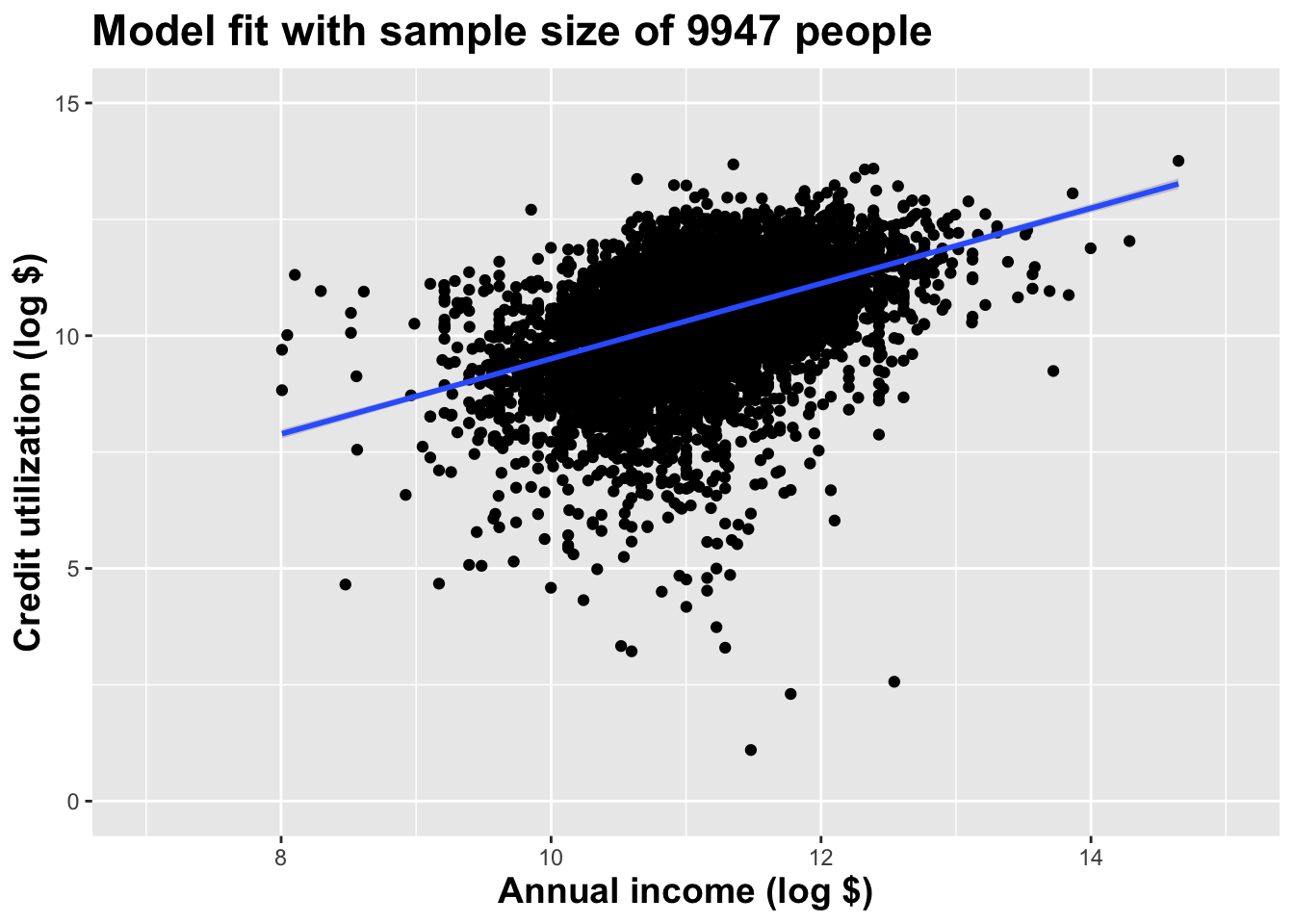

Double the sample size

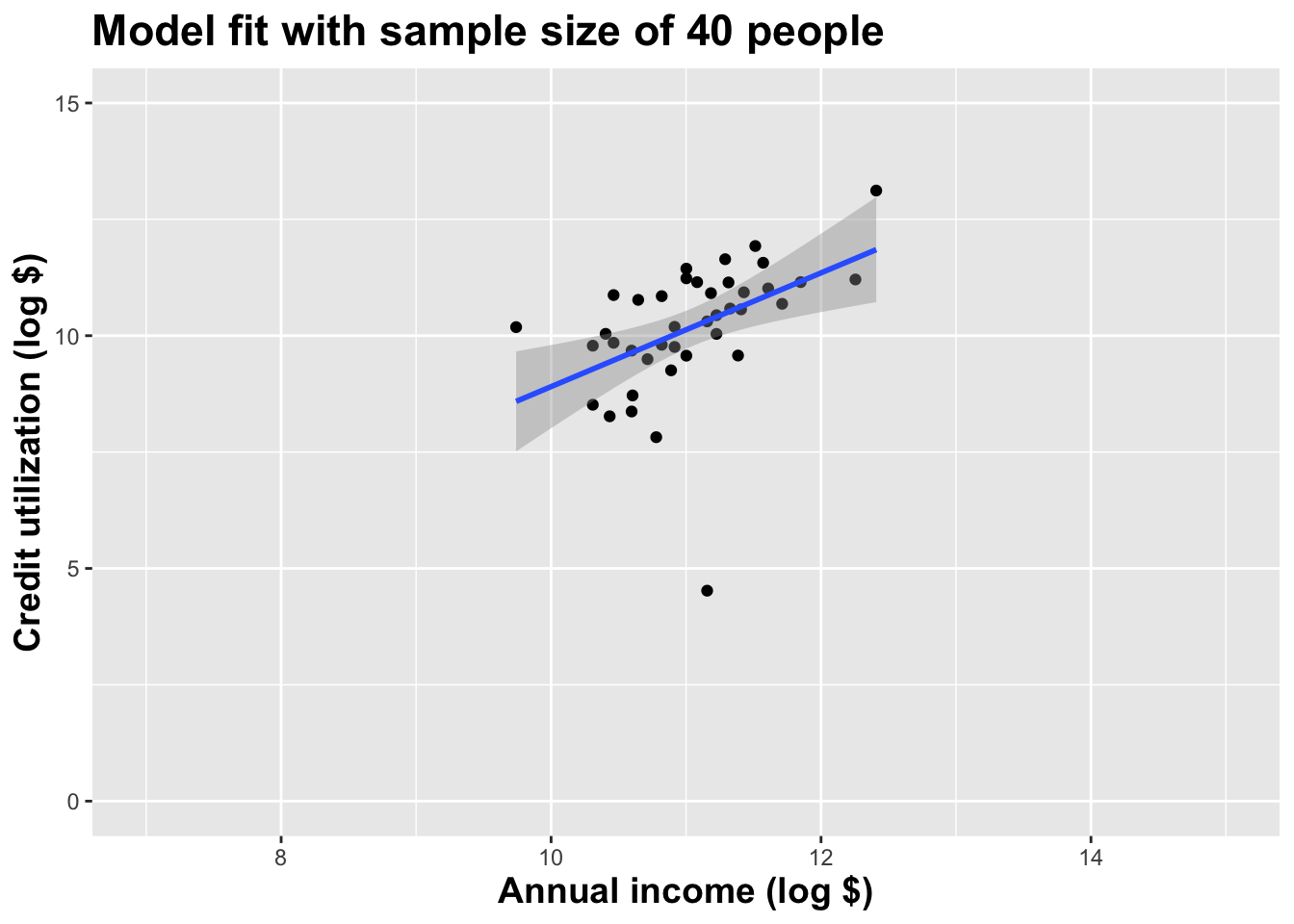

Double the sample size again

Double the sample size again

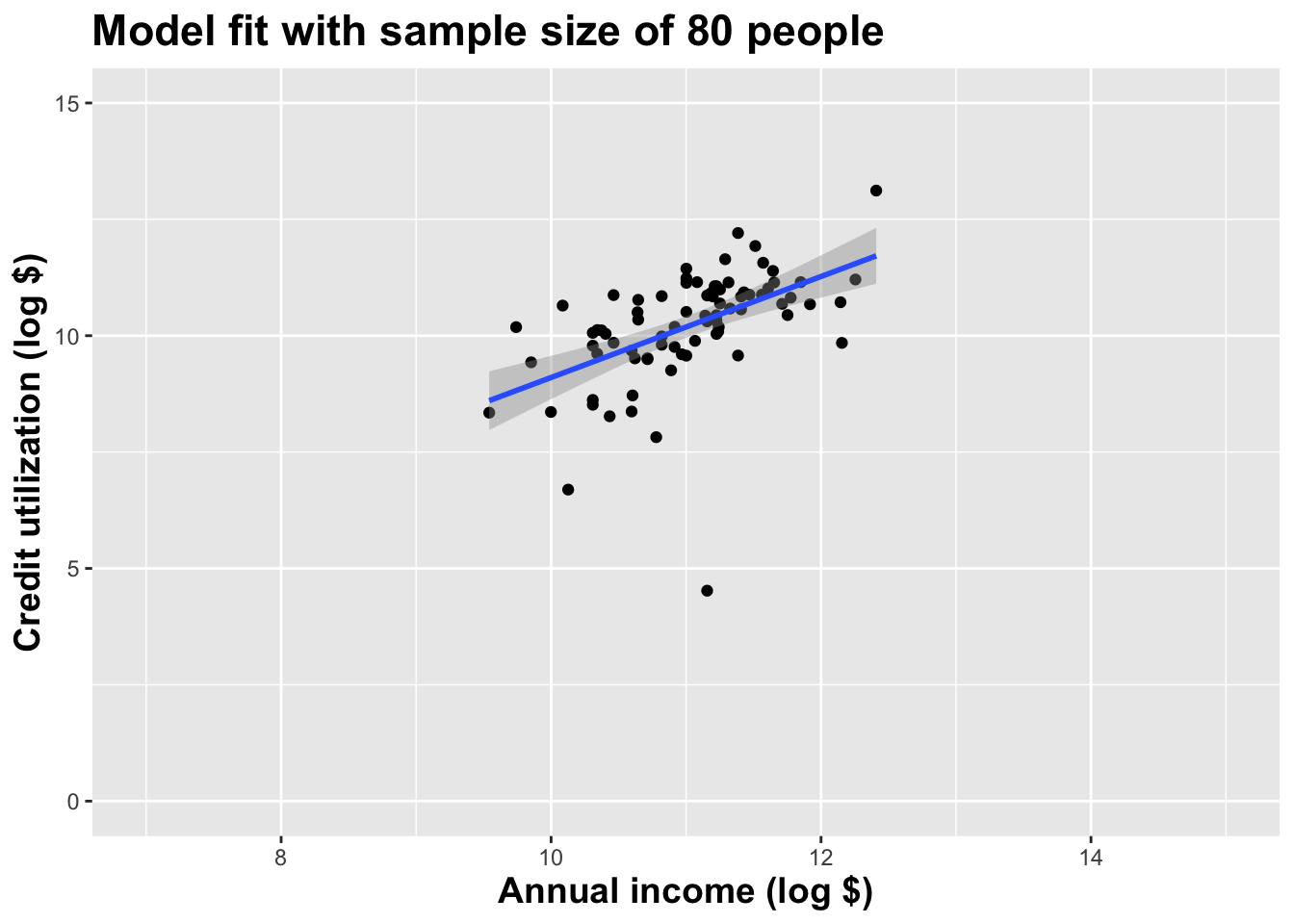

Double the sample size again

Double the sample size again

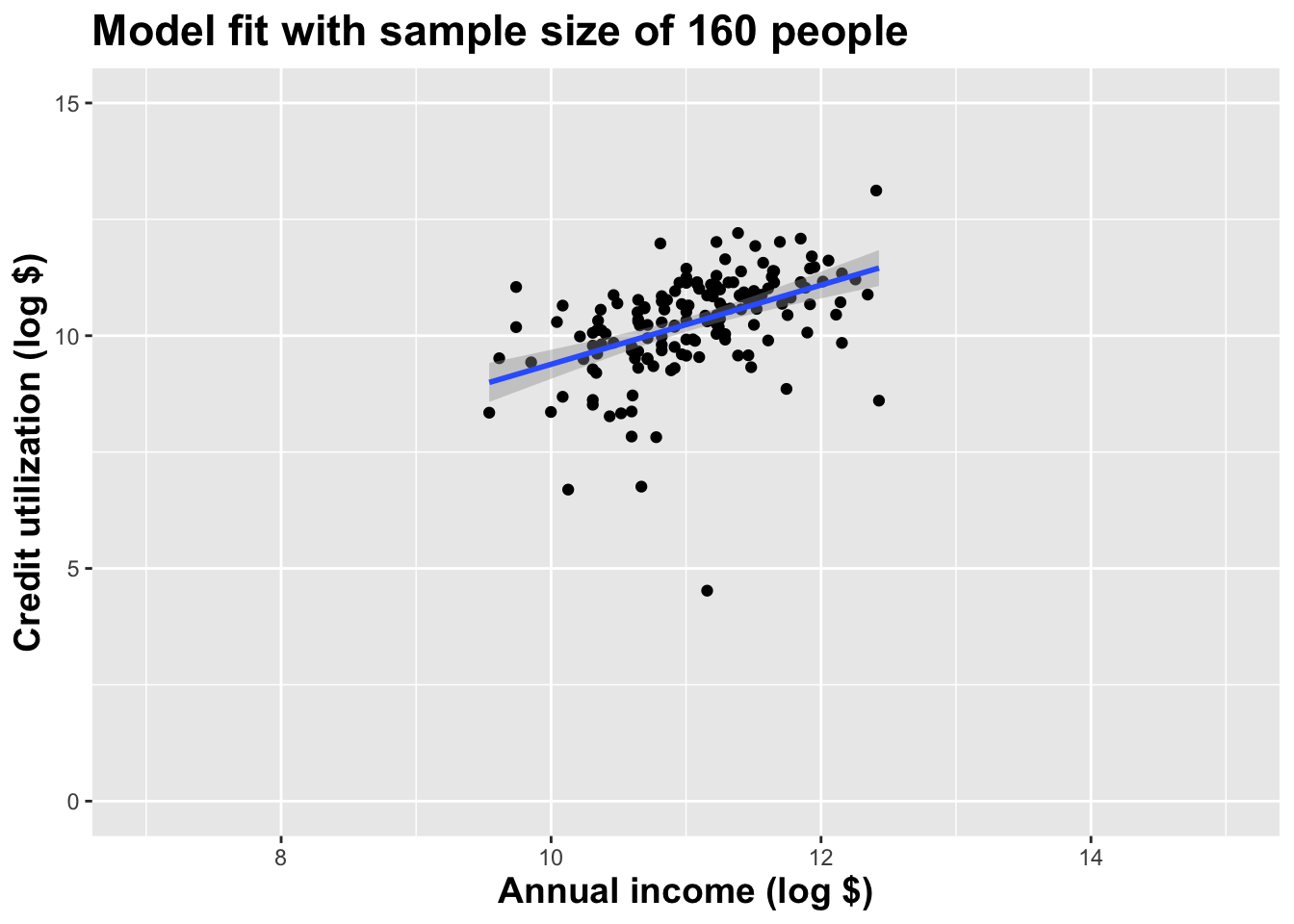

Double the sample size again

Double the sample size again

Double the sample size again

Double the sample size yet again

Double the sample size one more time

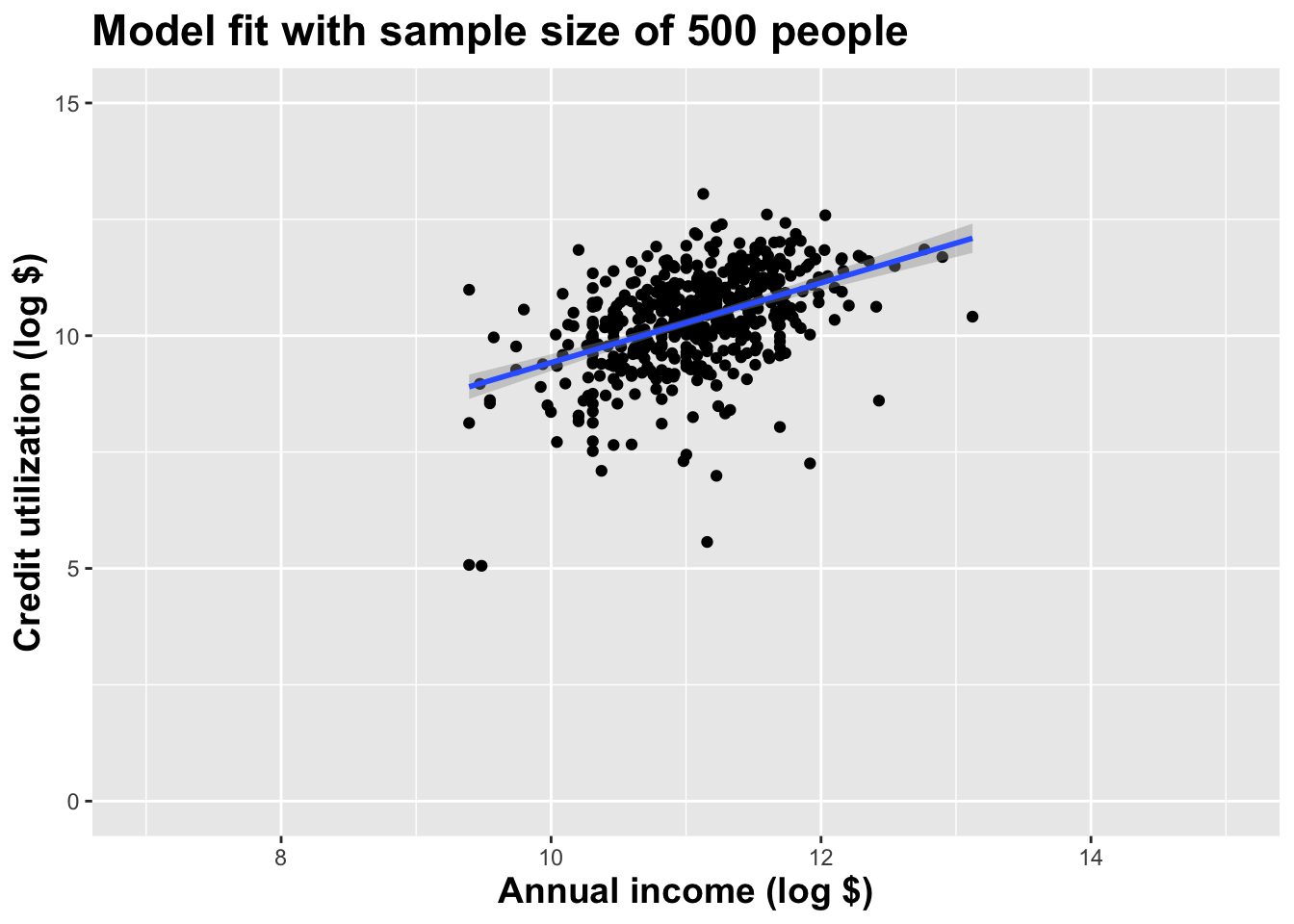

Use all the data we have

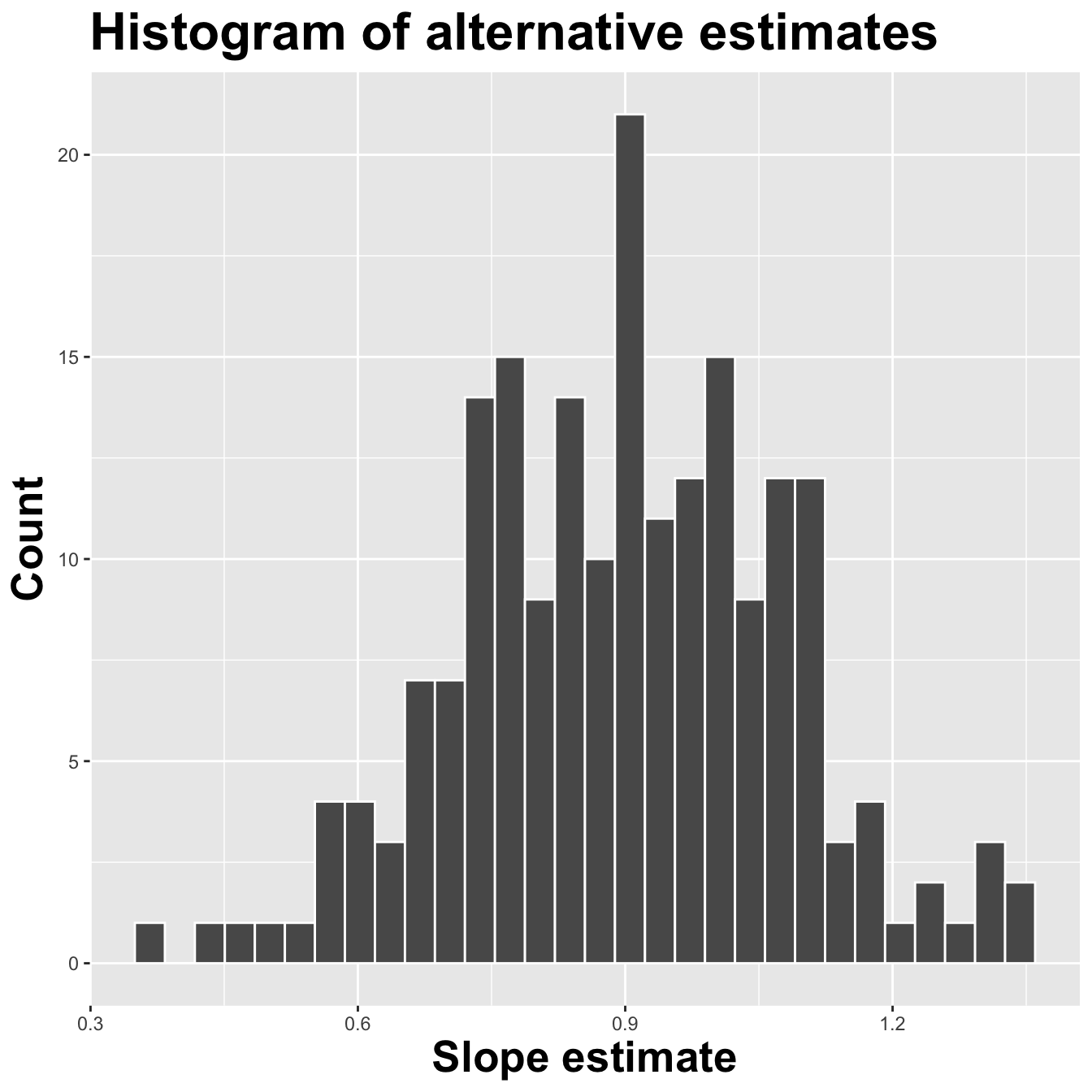

Here’s one dataset we could have seen

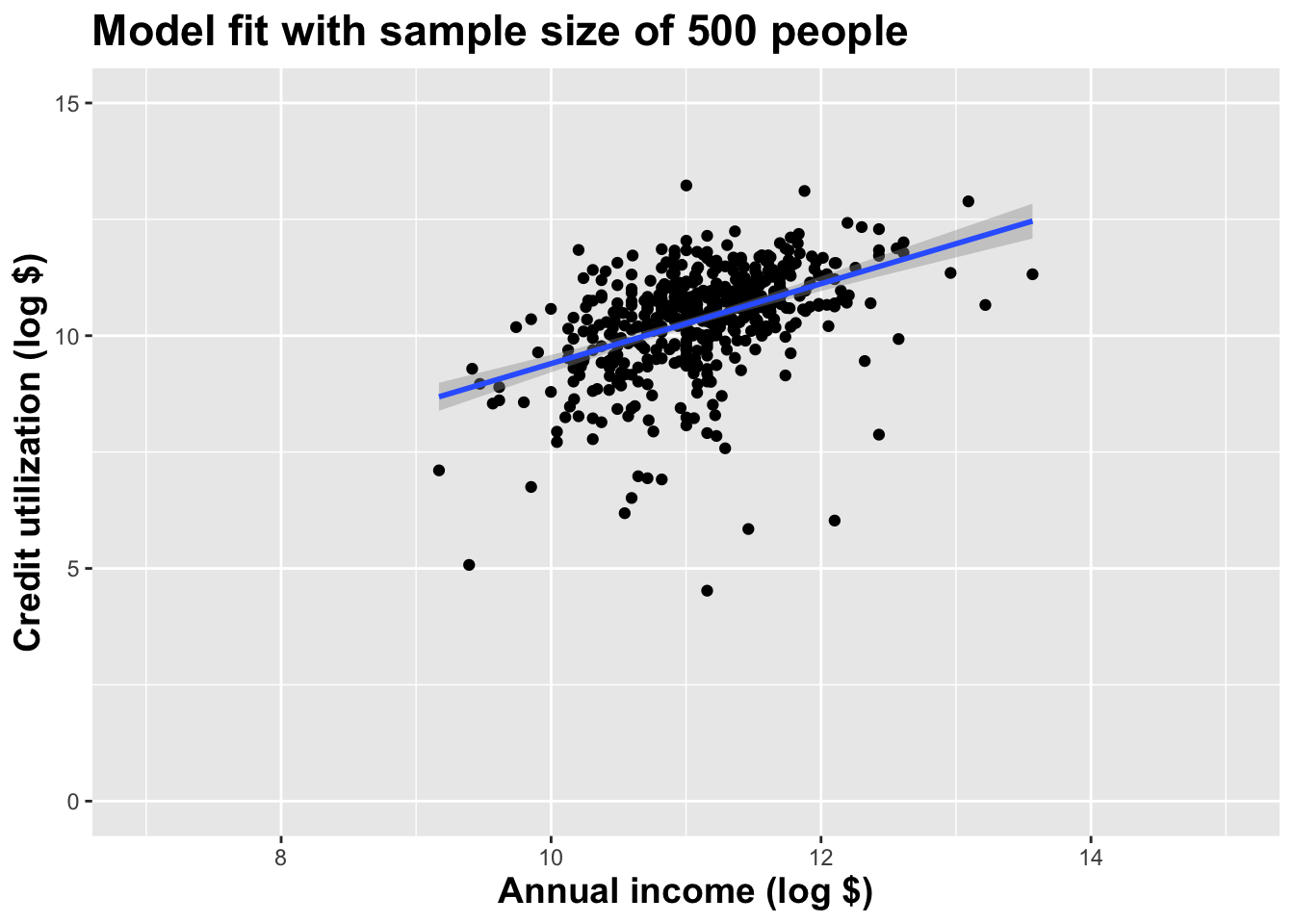

Here’s another

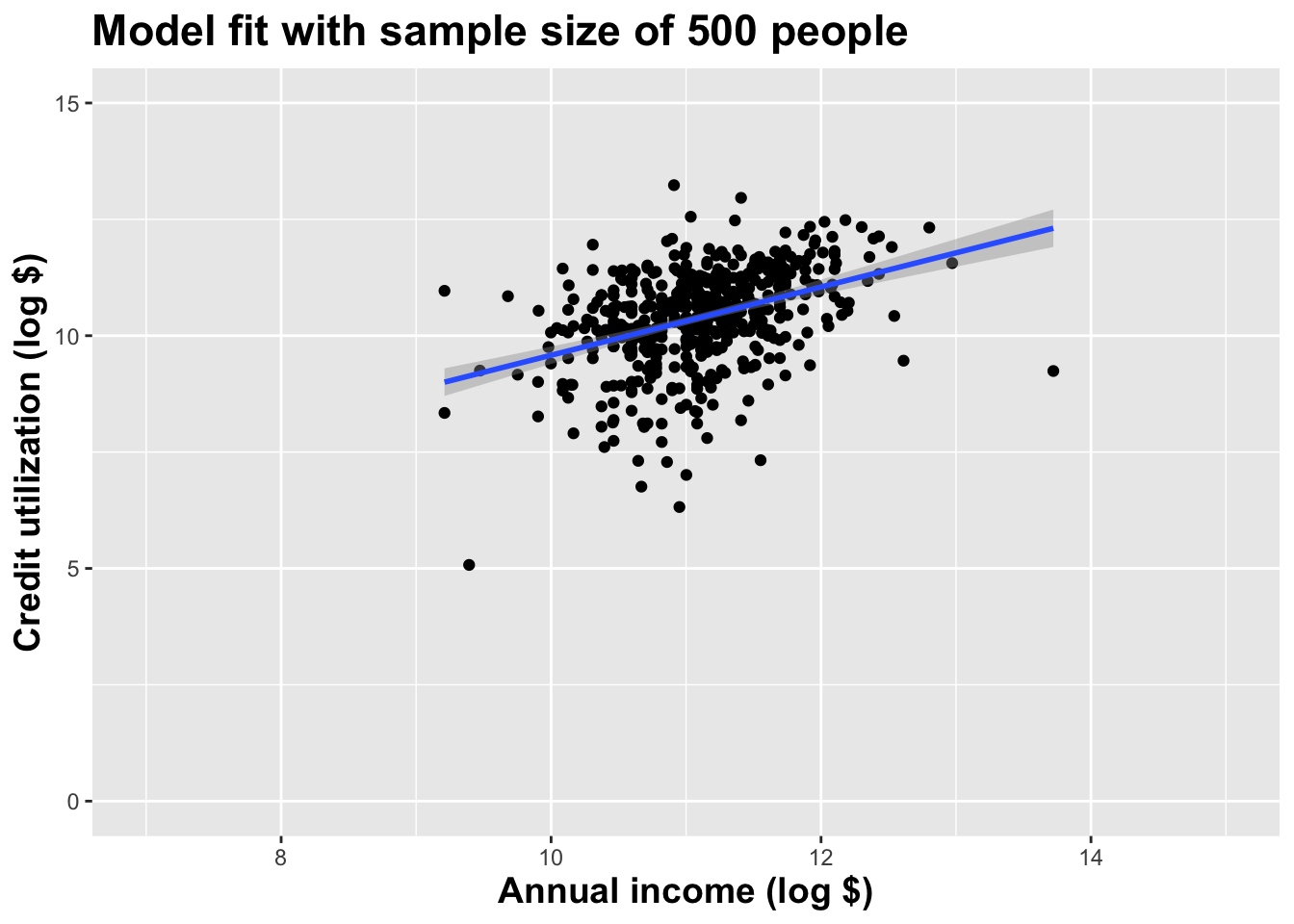

Here’s yet one more

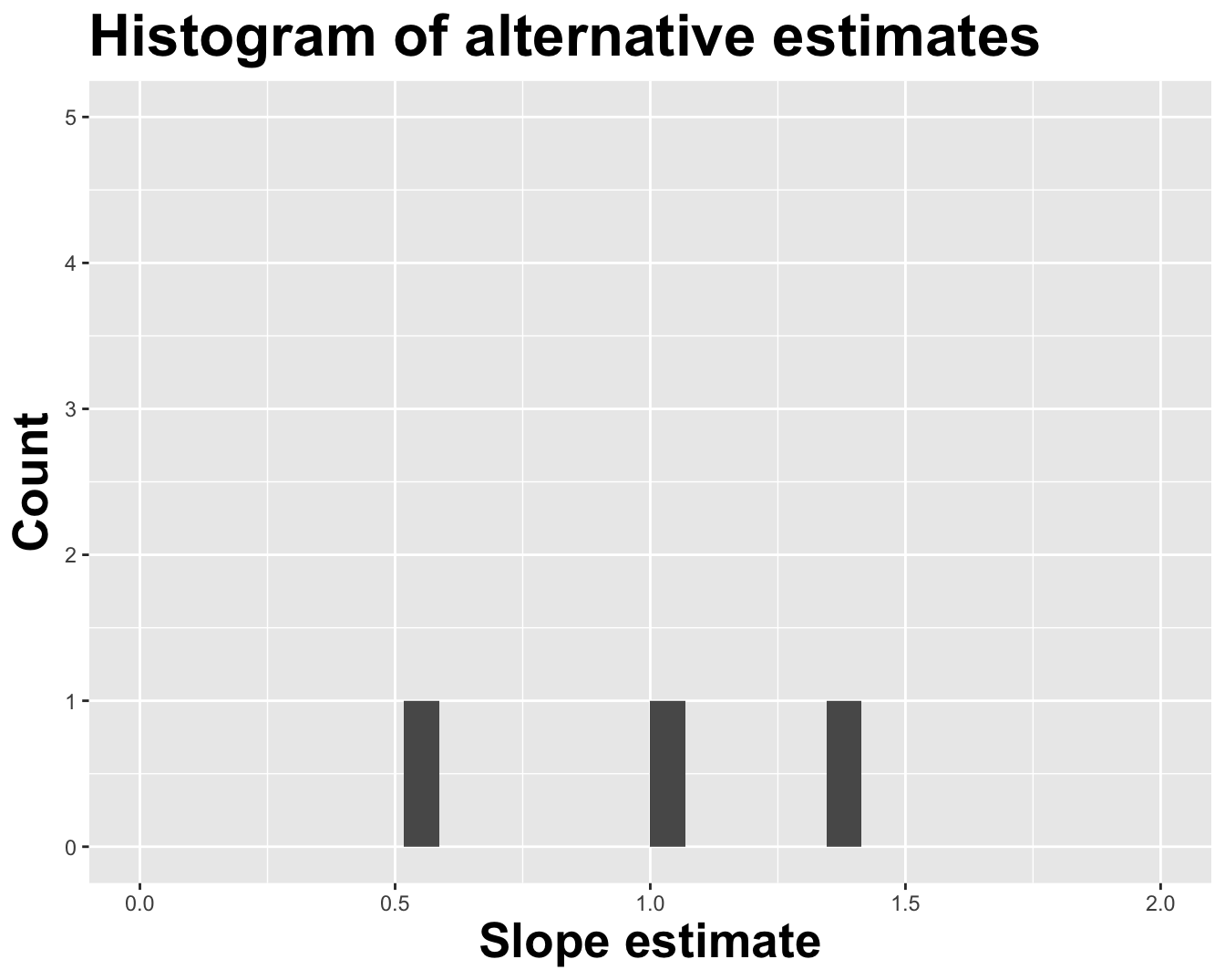

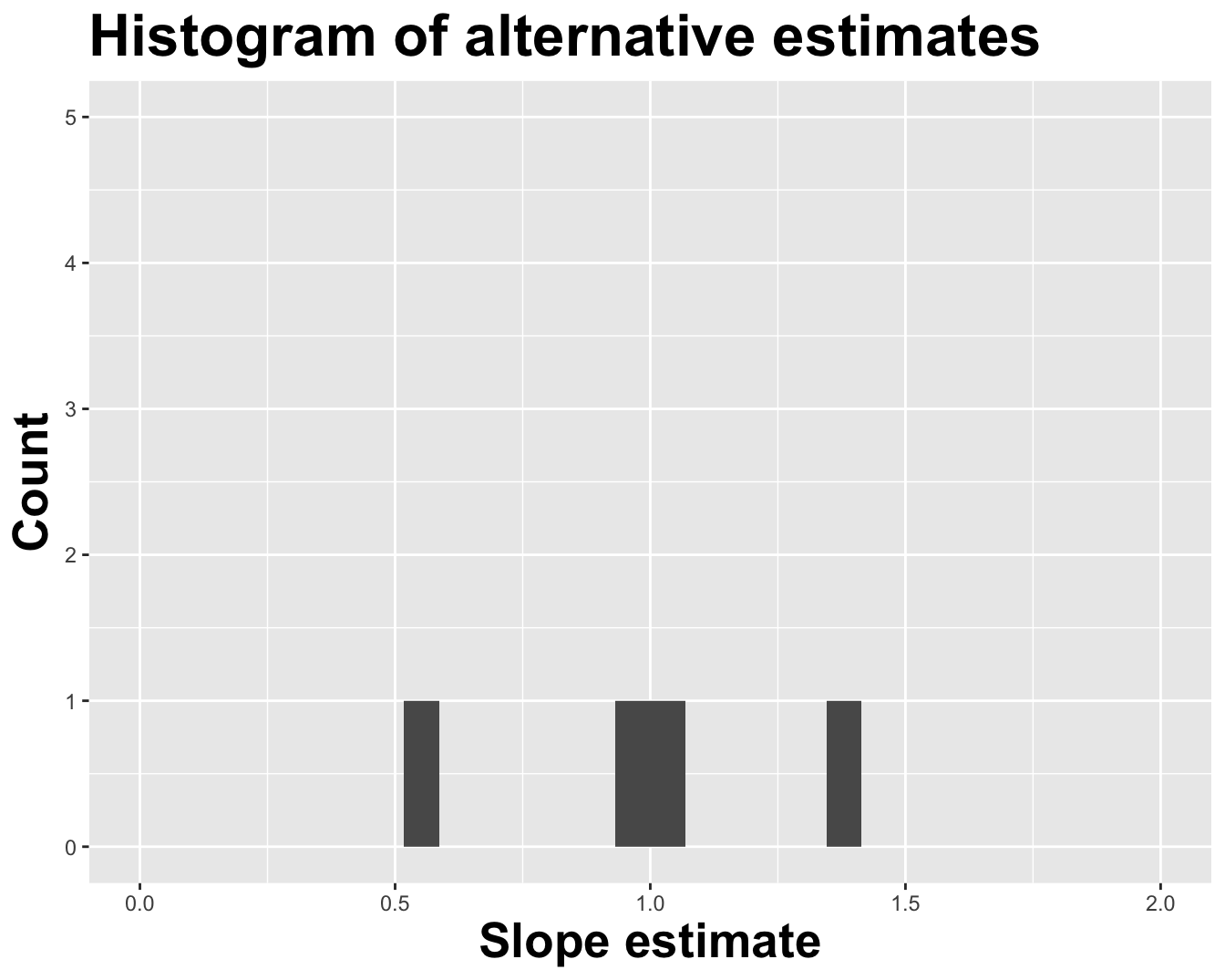

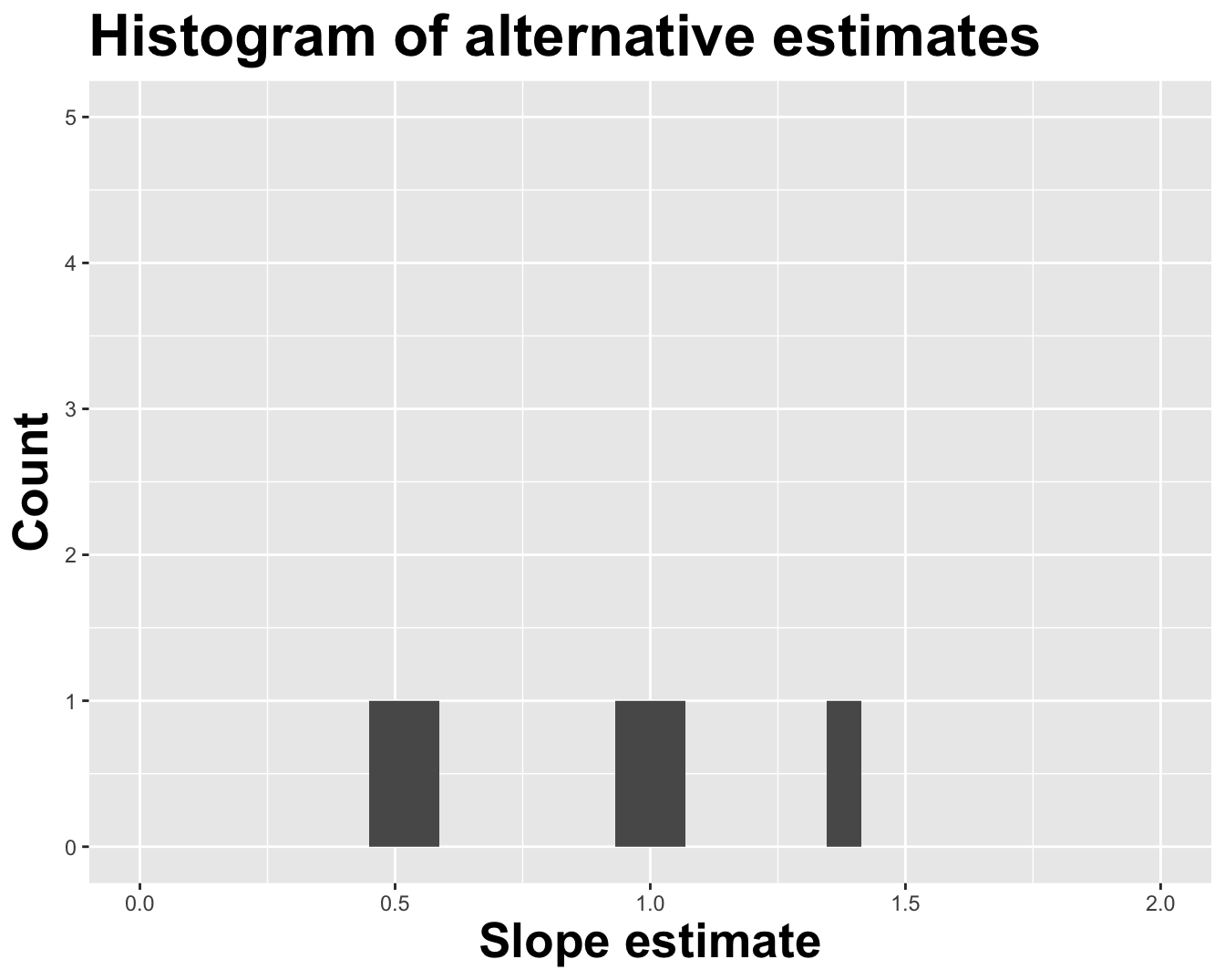

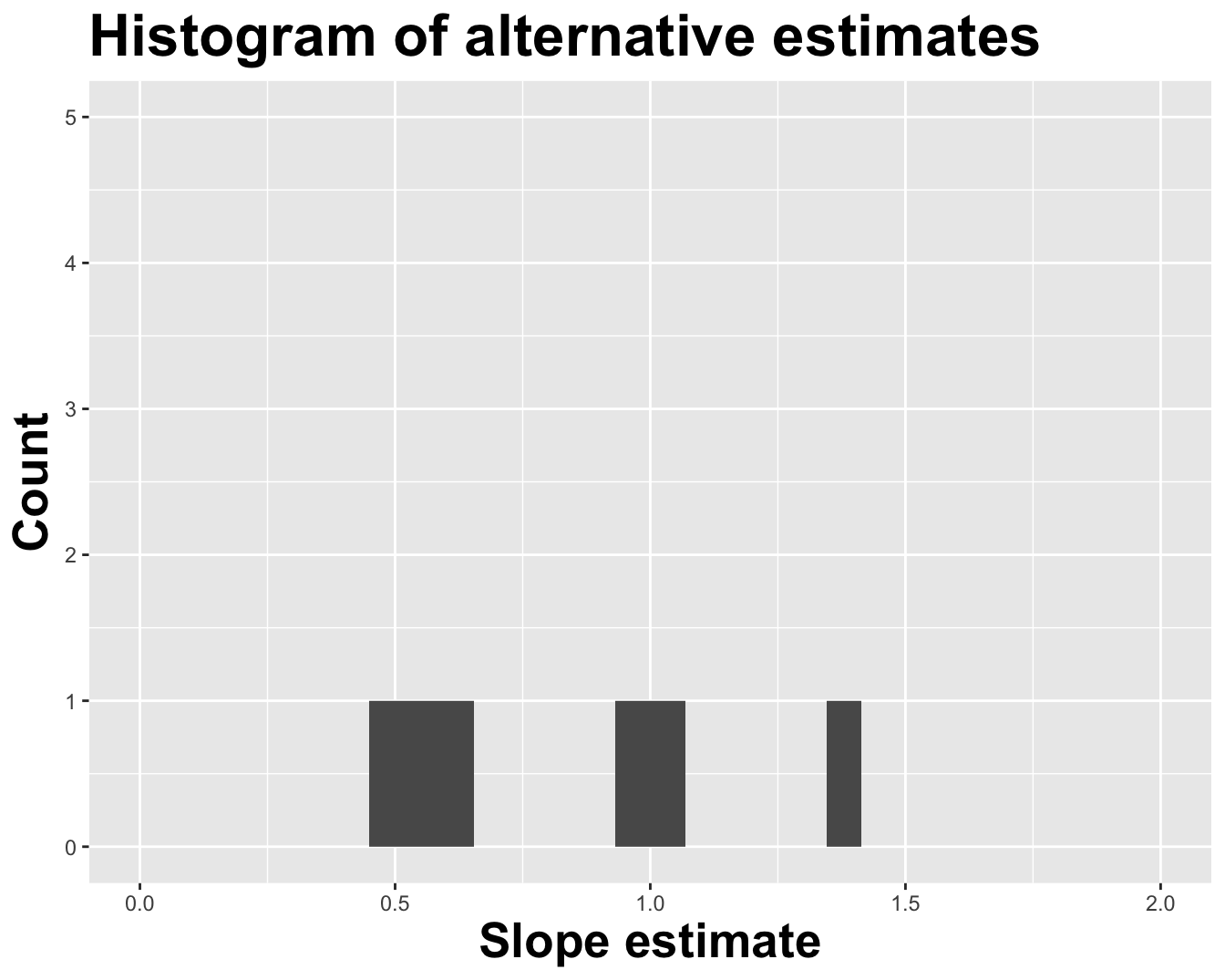

Alternative 1

Alternative 2

Alternative 3

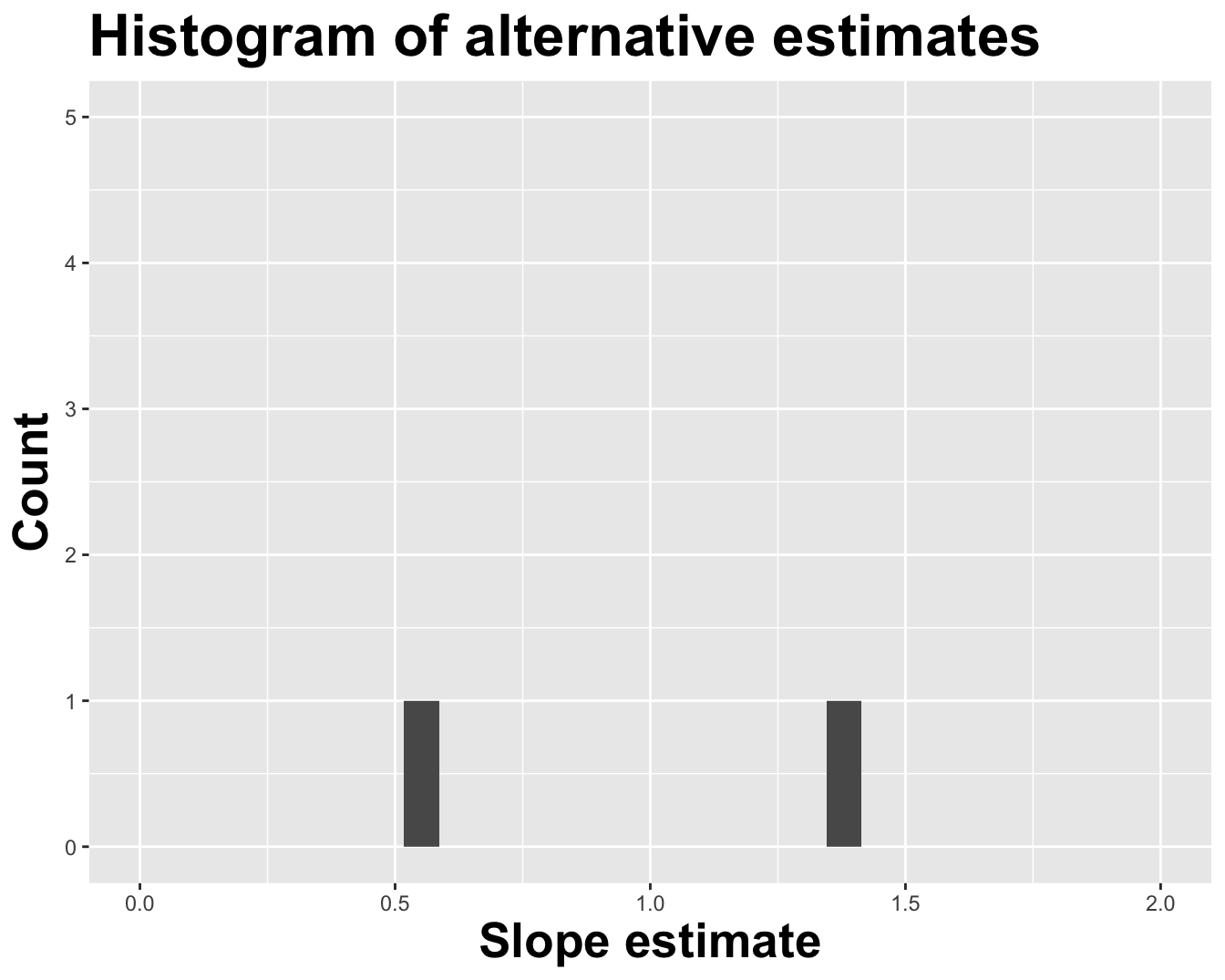

Different data set -> different estimates

# A tibble: 2 × 2

term estimate

<chr> <dbl>

1 (Intercept) 4.27

2 log_inc 0.553

Different data set -> different estimates

# A tibble: 2 × 2

term estimate

<chr> <dbl>

1 (Intercept) -4.63

2 log_inc 1.35

Different data set -> different estimates

# A tibble: 2 × 2

term estimate

<chr> <dbl>

1 (Intercept) -1.14

2 log_inc 1.04

Different data set -> different estimates

# A tibble: 2 × 2

term estimate

<chr> <dbl>

1 (Intercept) -0.288

2 log_inc 0.960

Different data set -> different estimates

# A tibble: 2 × 2

term estimate

<chr> <dbl>

1 (Intercept) 4.84

2 log_inc 0.492

Different data set -> different estimates

# A tibble: 2 × 2

term estimate

<chr> <dbl>

1 (Intercept) 3.20

2 log_inc 0.654

You get the idea

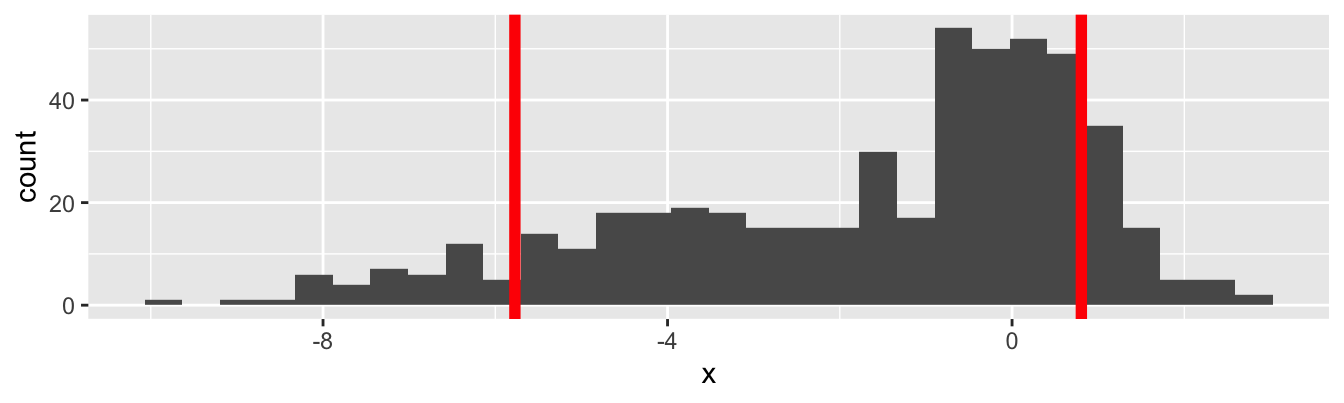

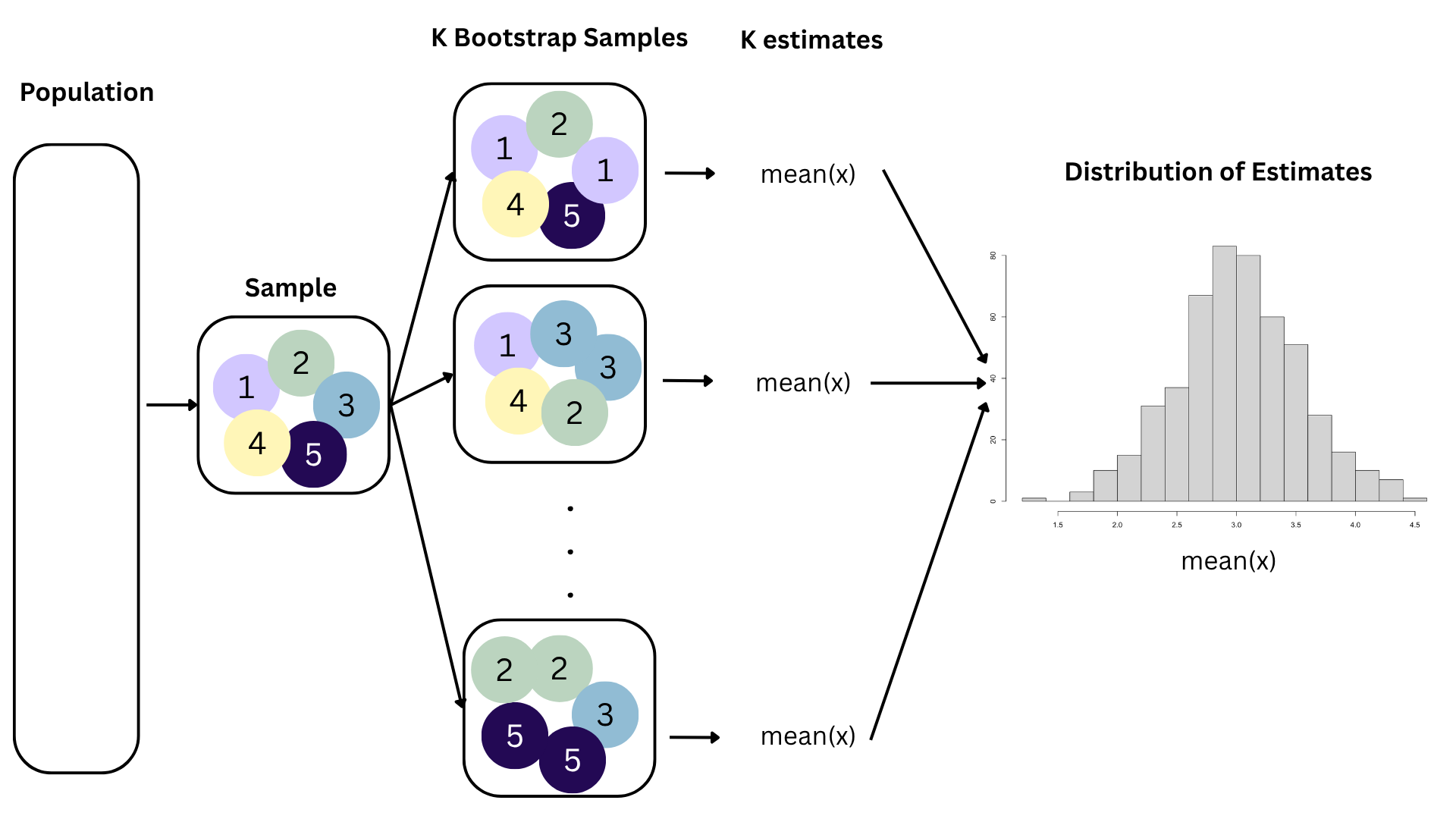

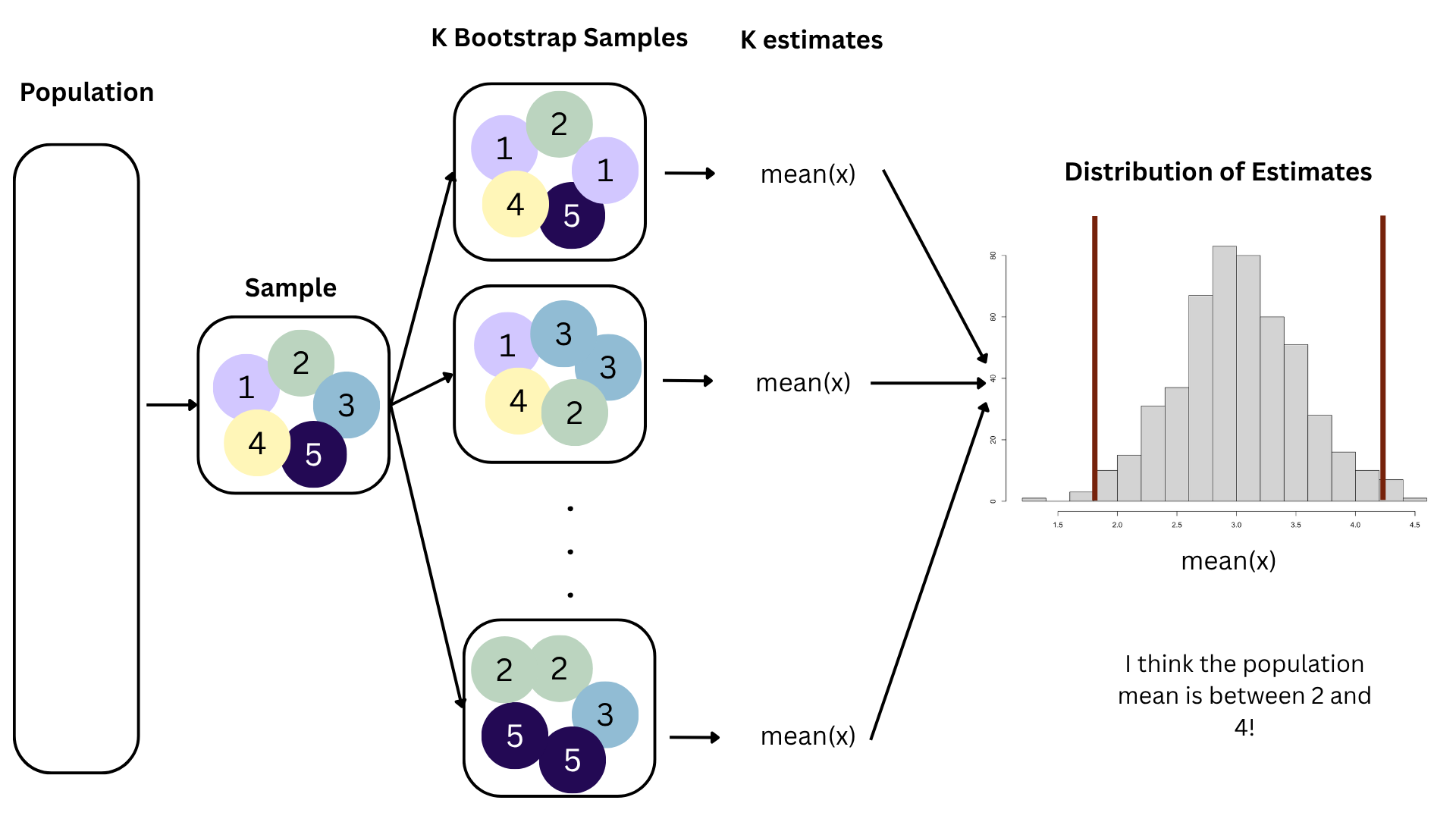

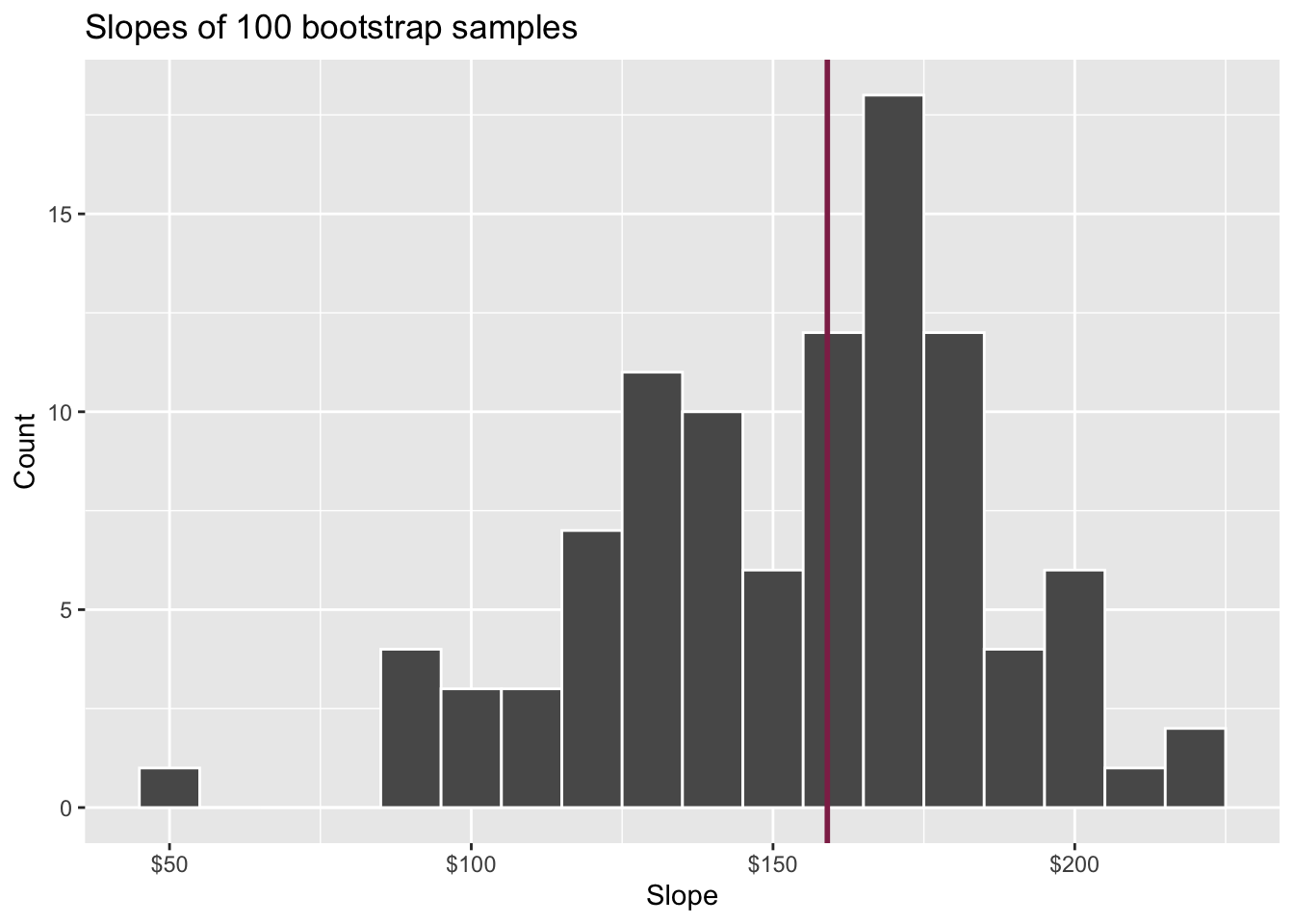

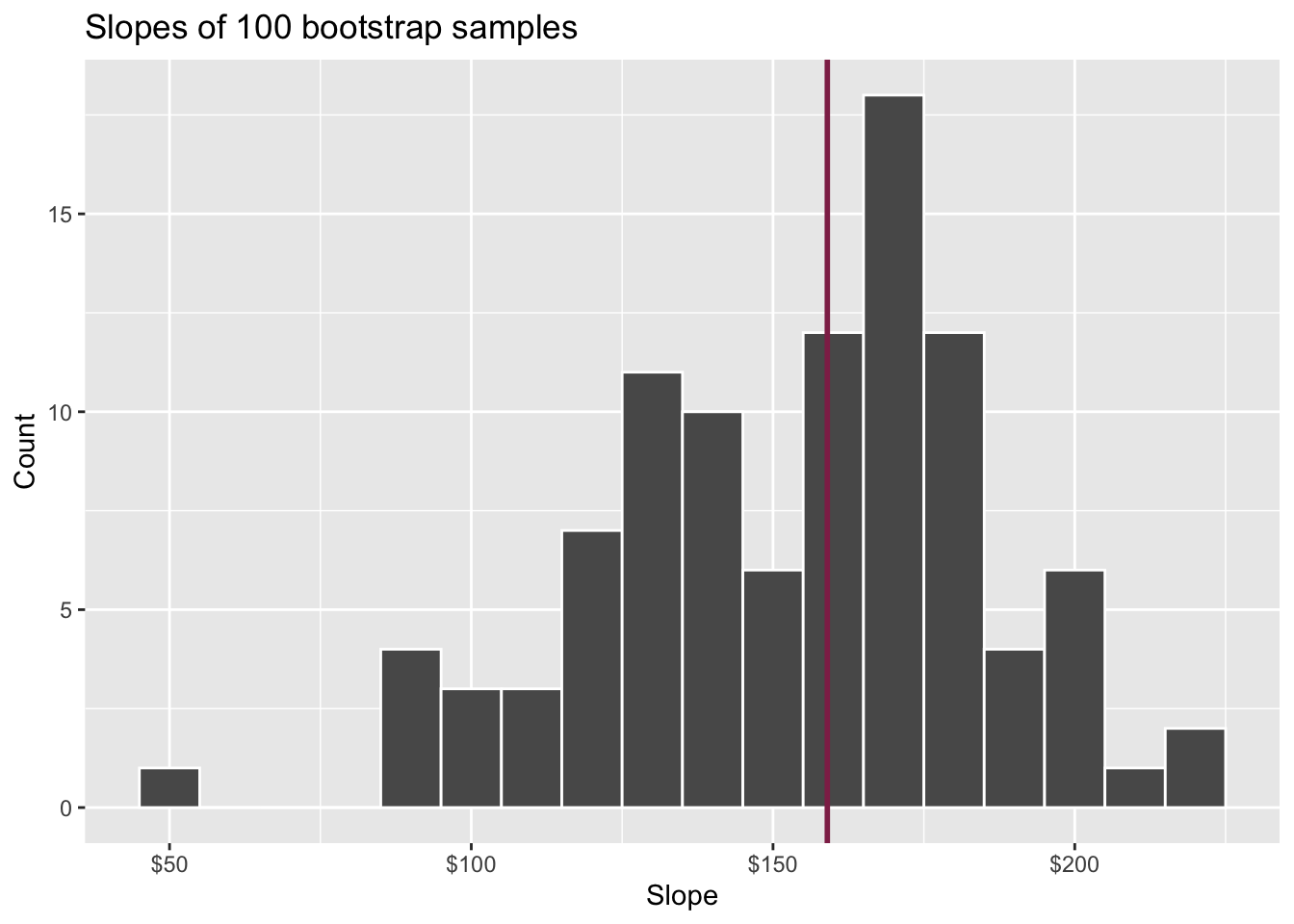

Variation in estimates across alternative datasets

The amount of variation in the histogram tells us something about the uncertainty, and gives us a range of likely values.

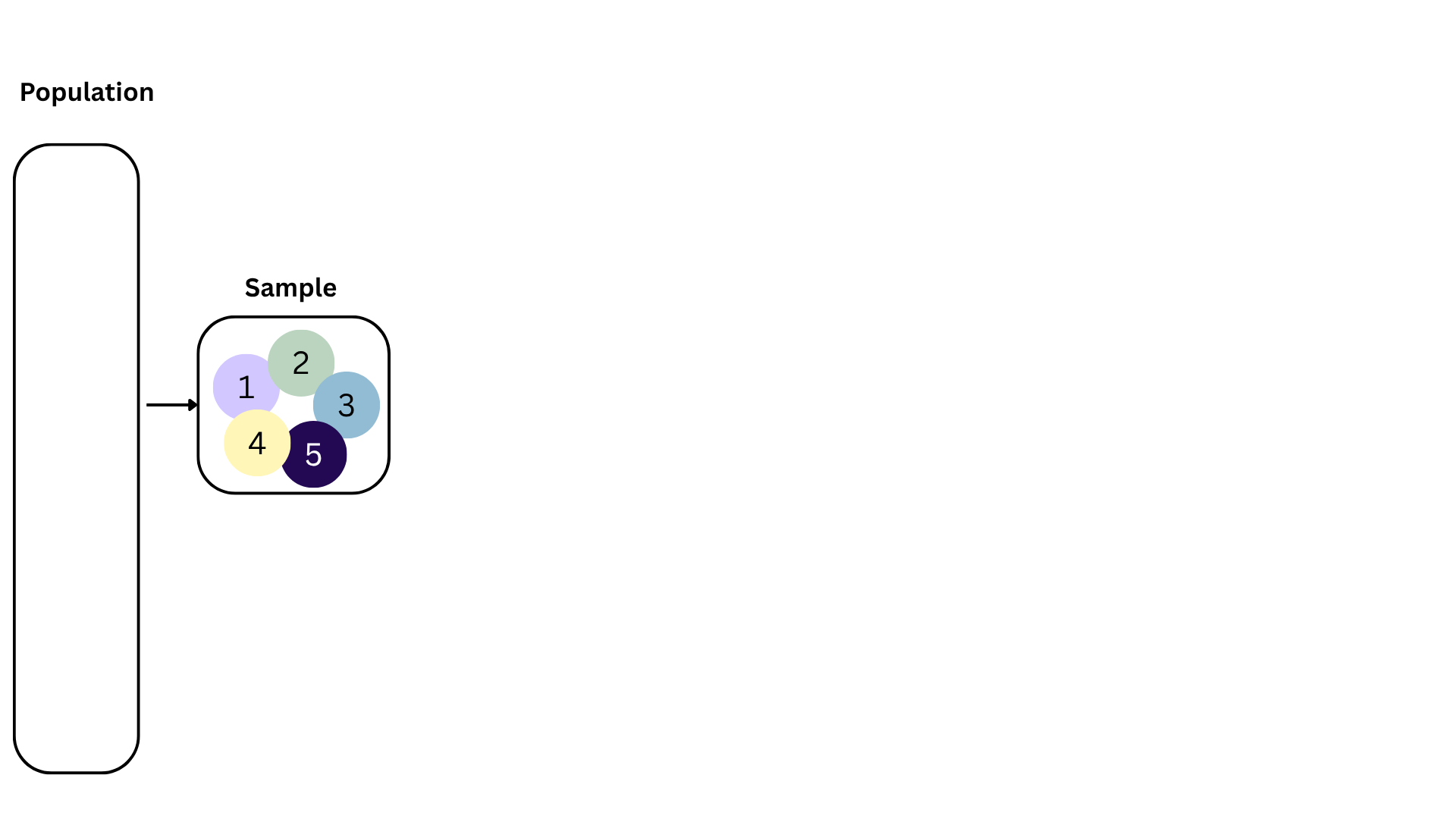

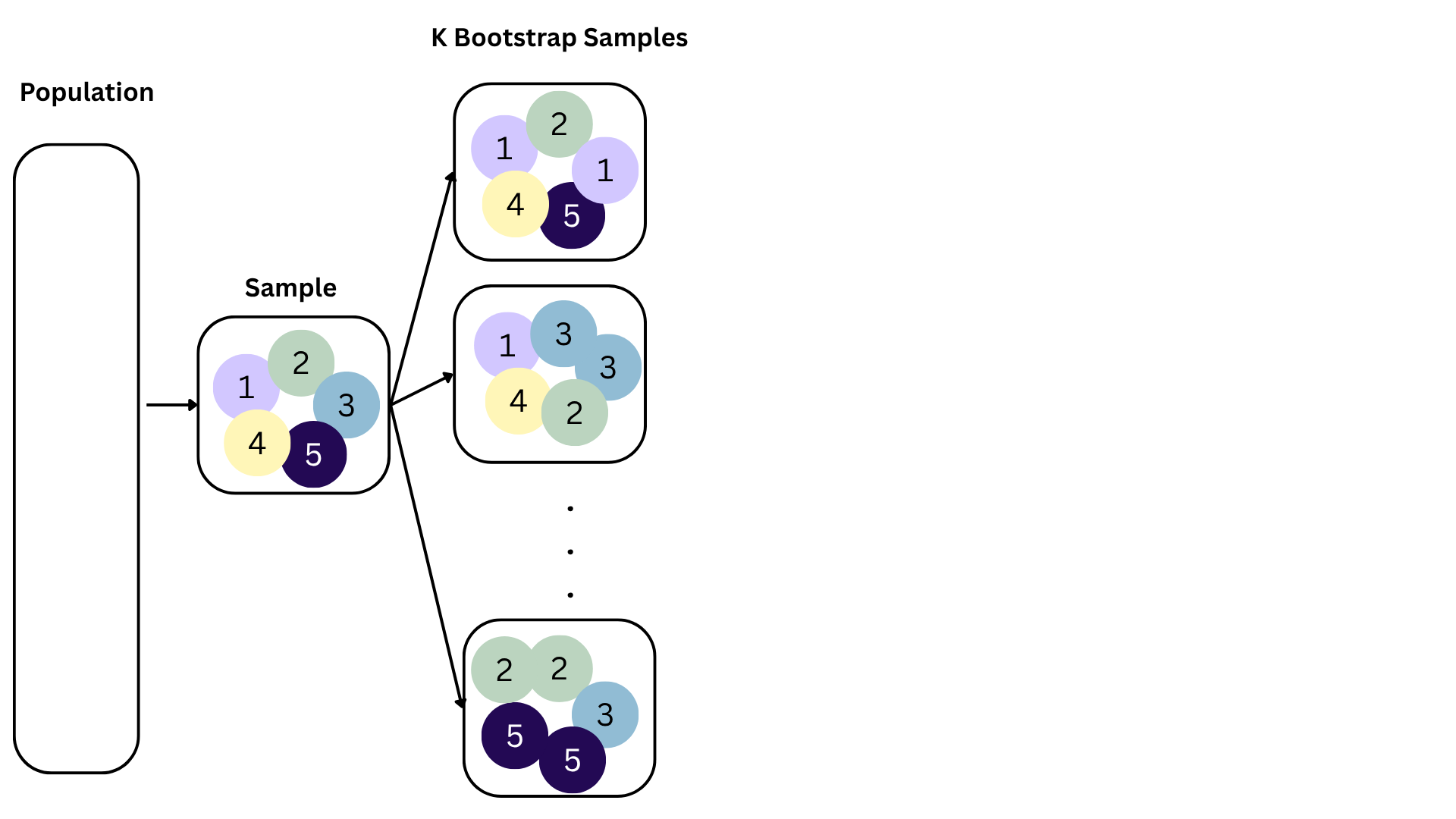

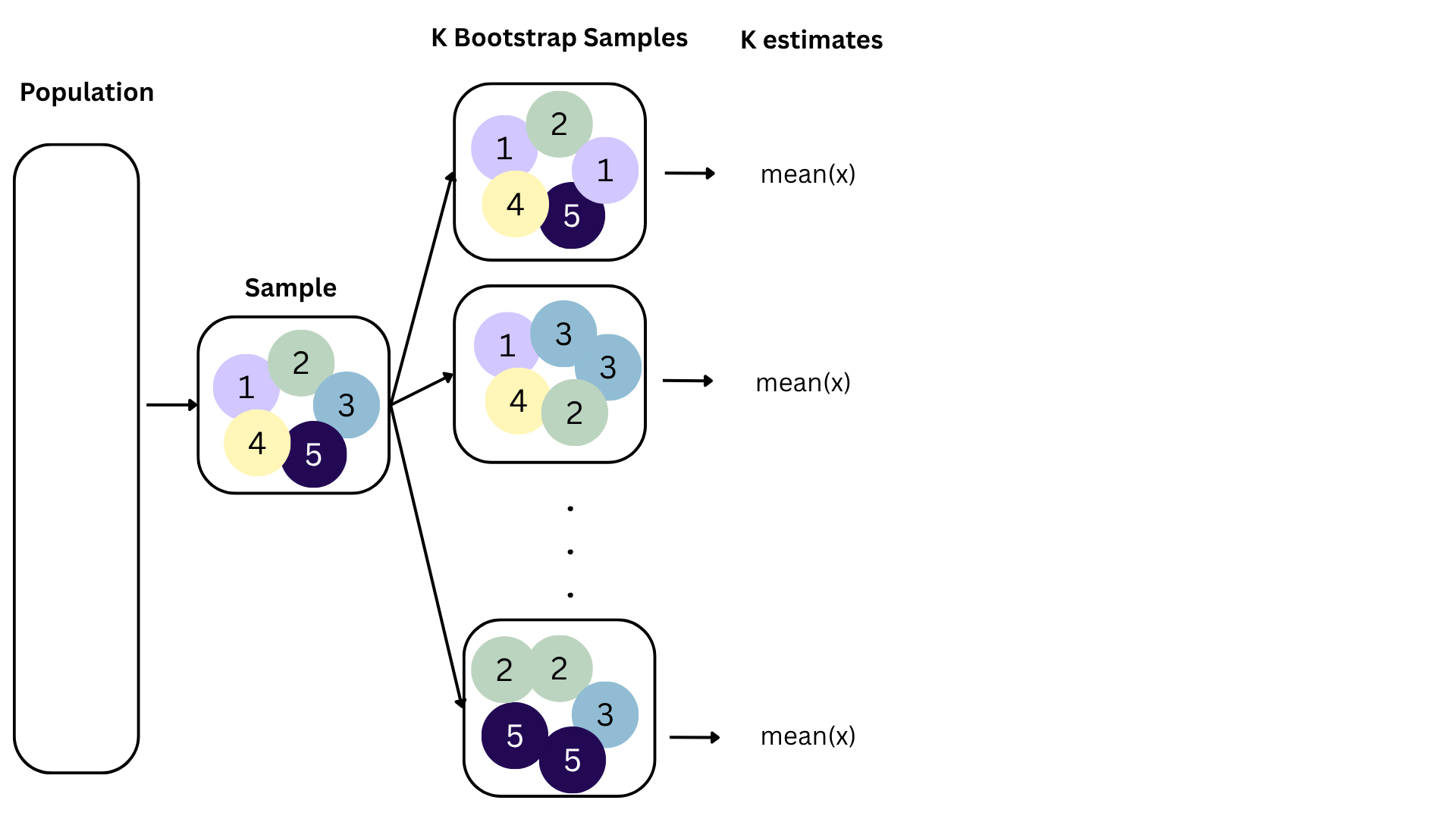

Bootstrapping

Bootstrapping

Bootstrapping

Bootstrapping

Bootstrapping

Bootstrapping

Bootstrapping

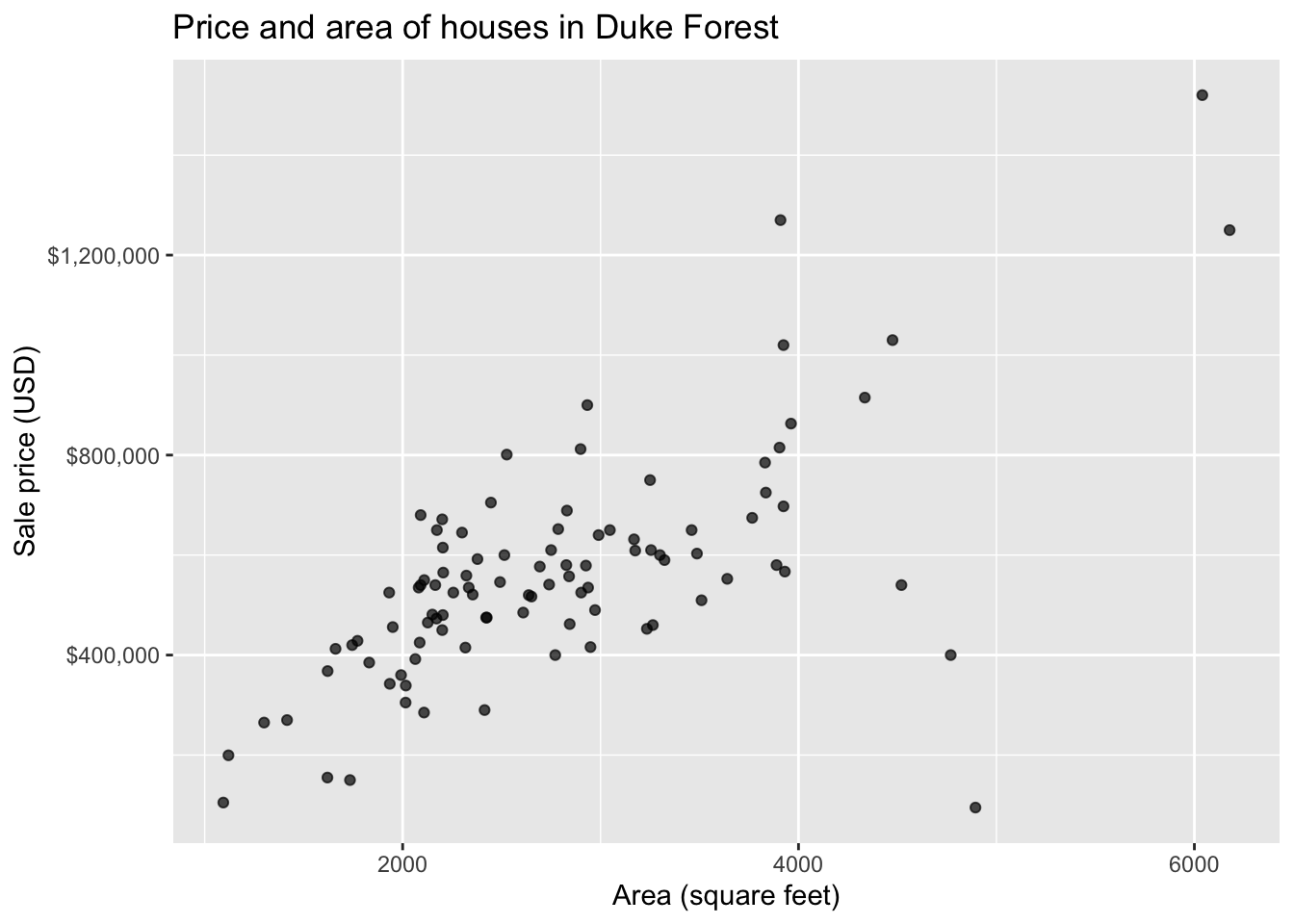

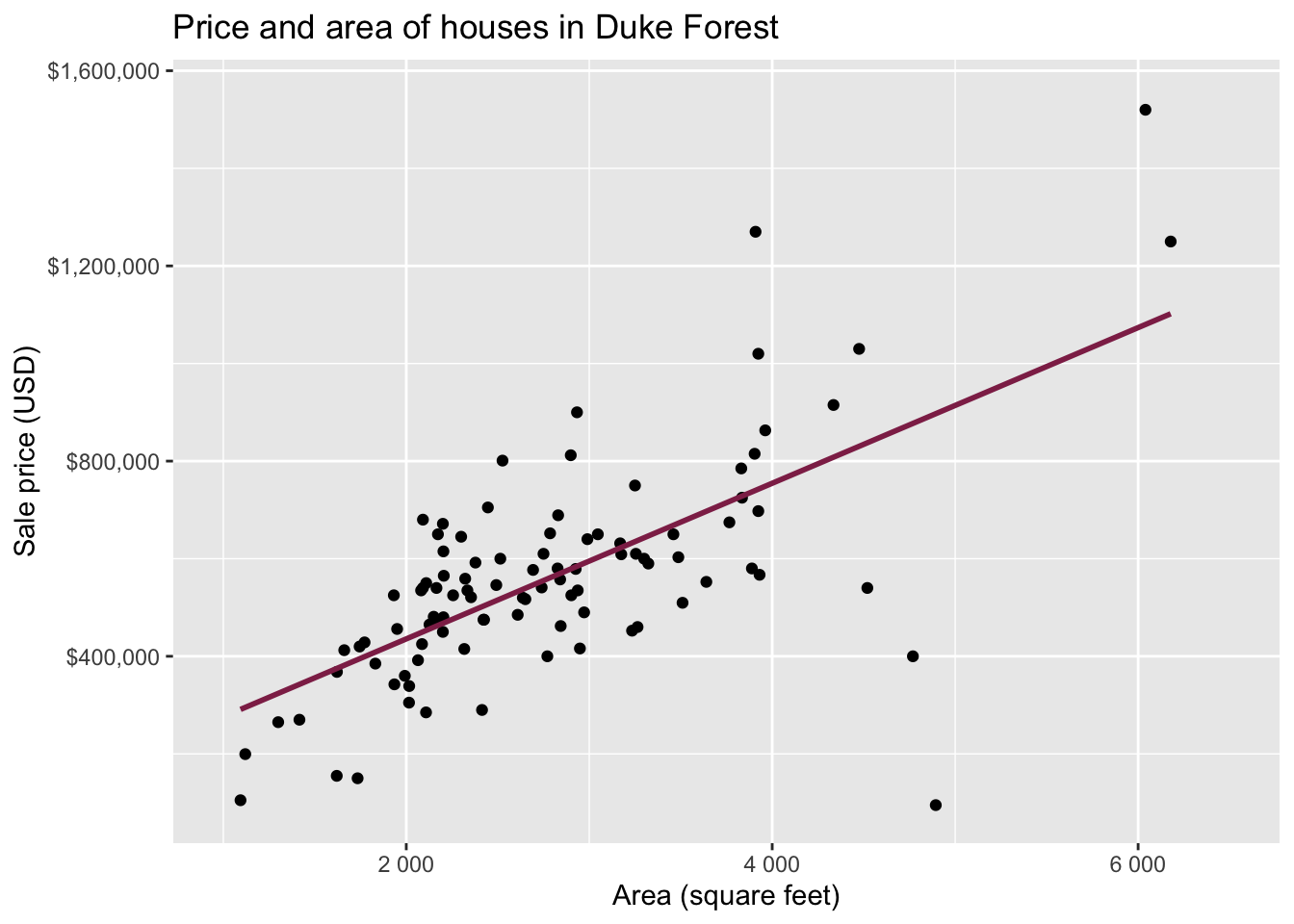

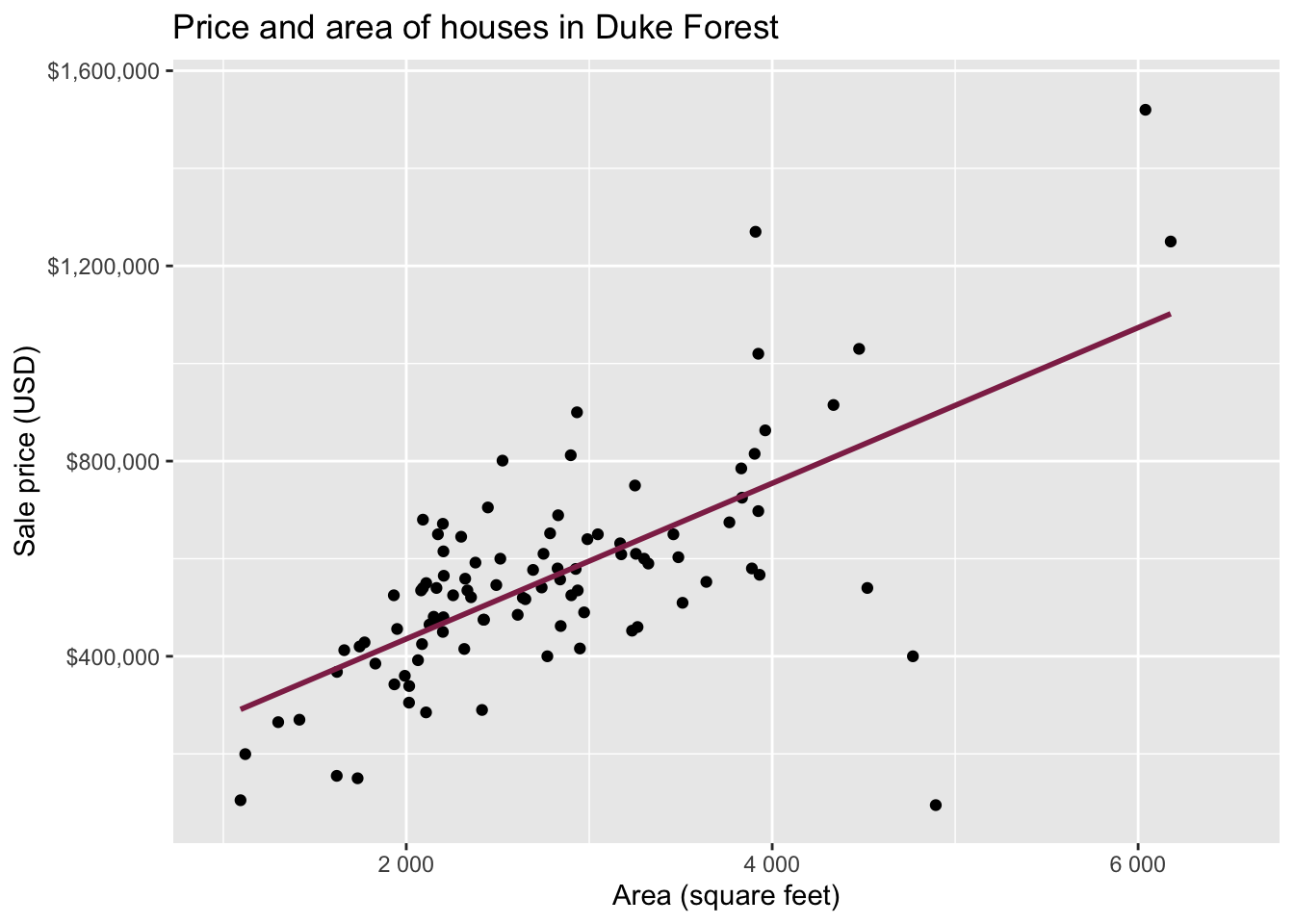

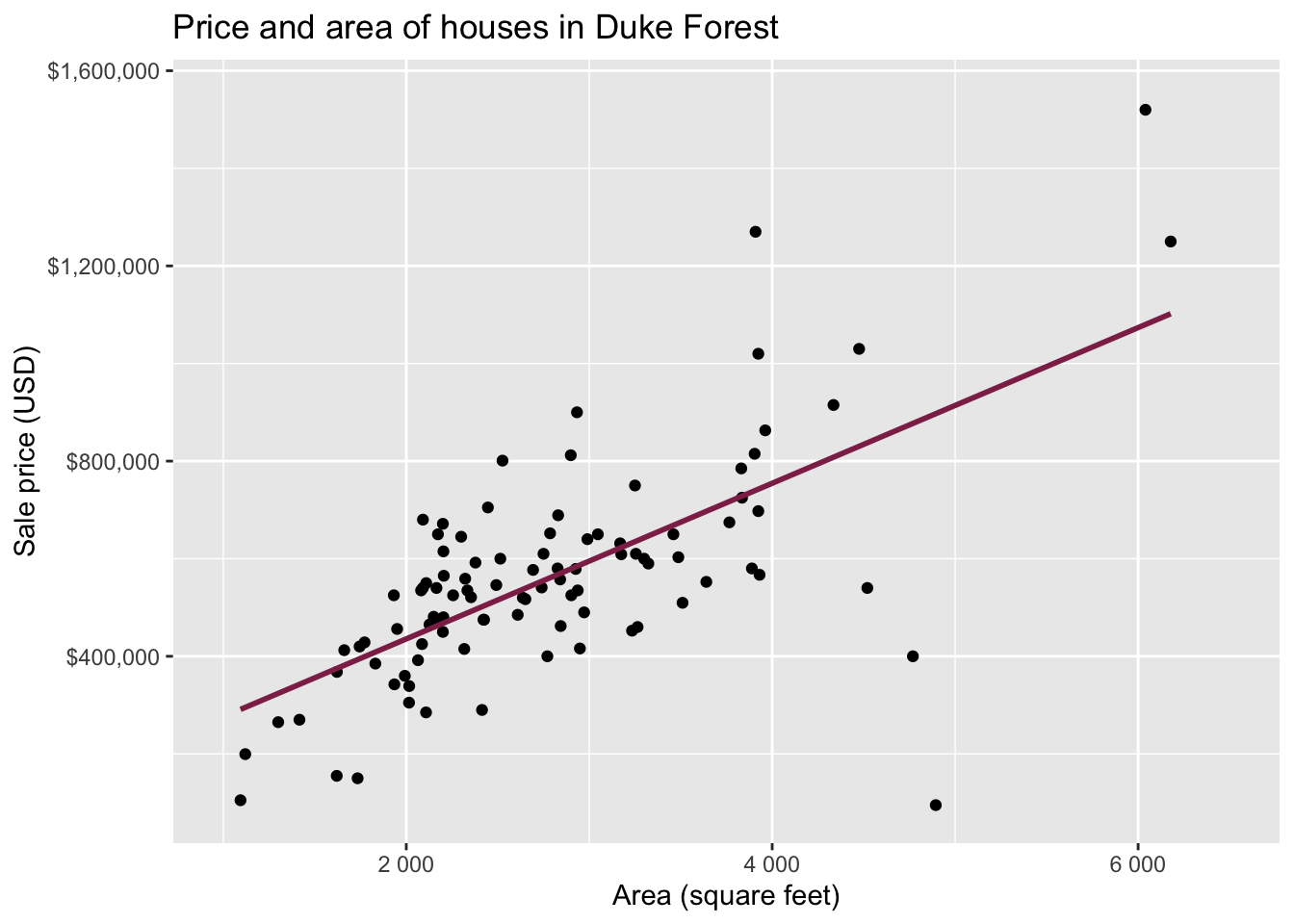

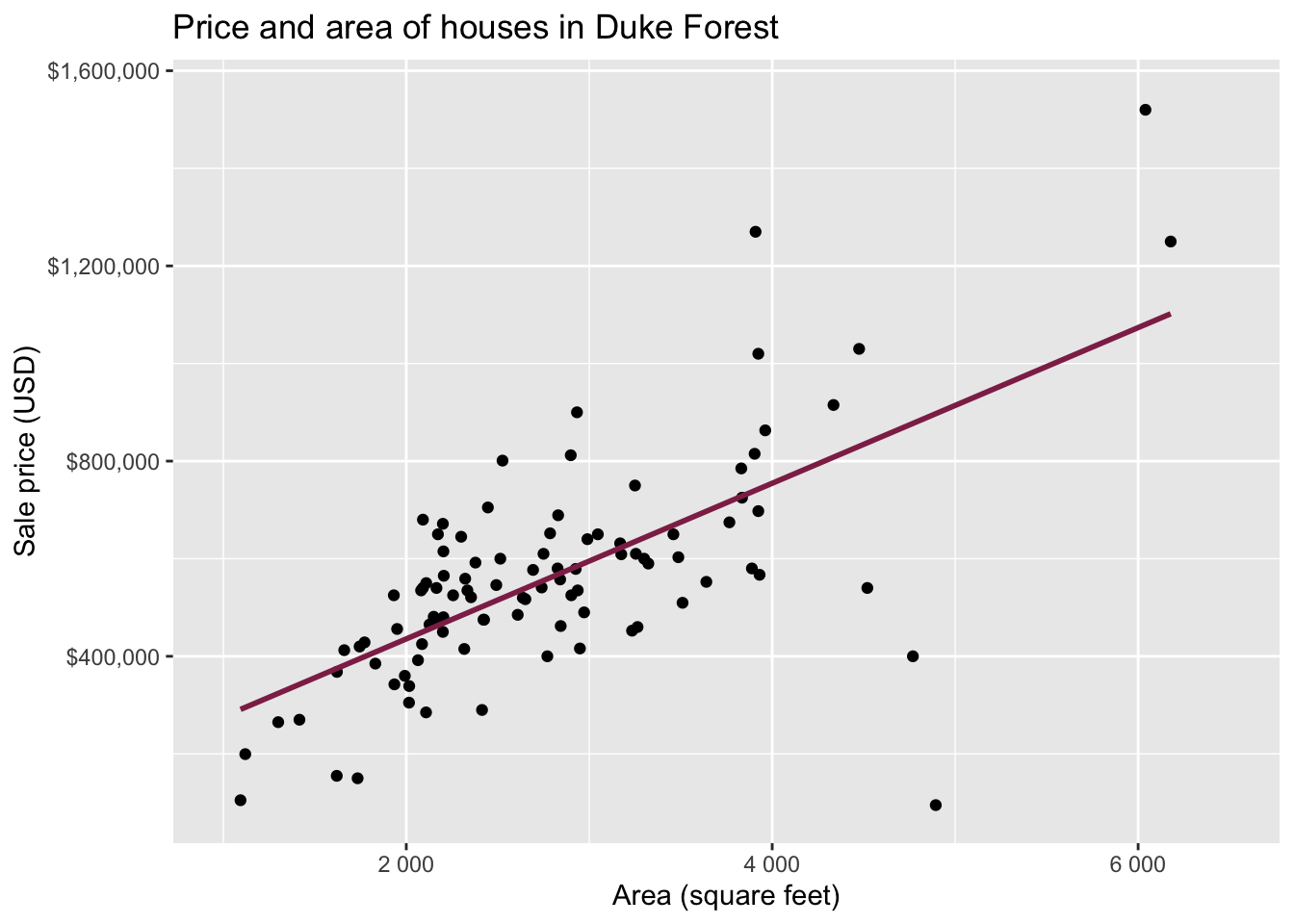

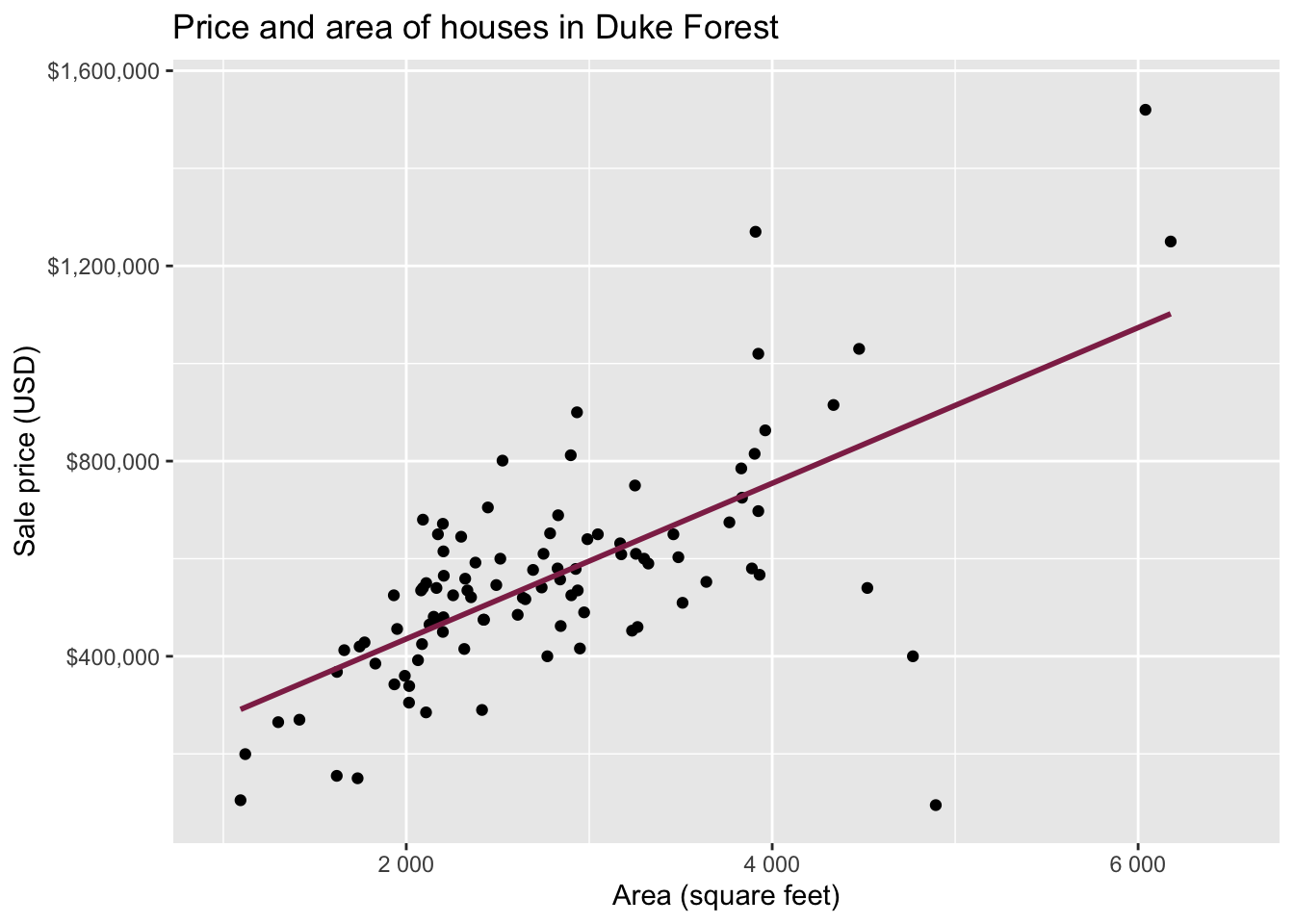

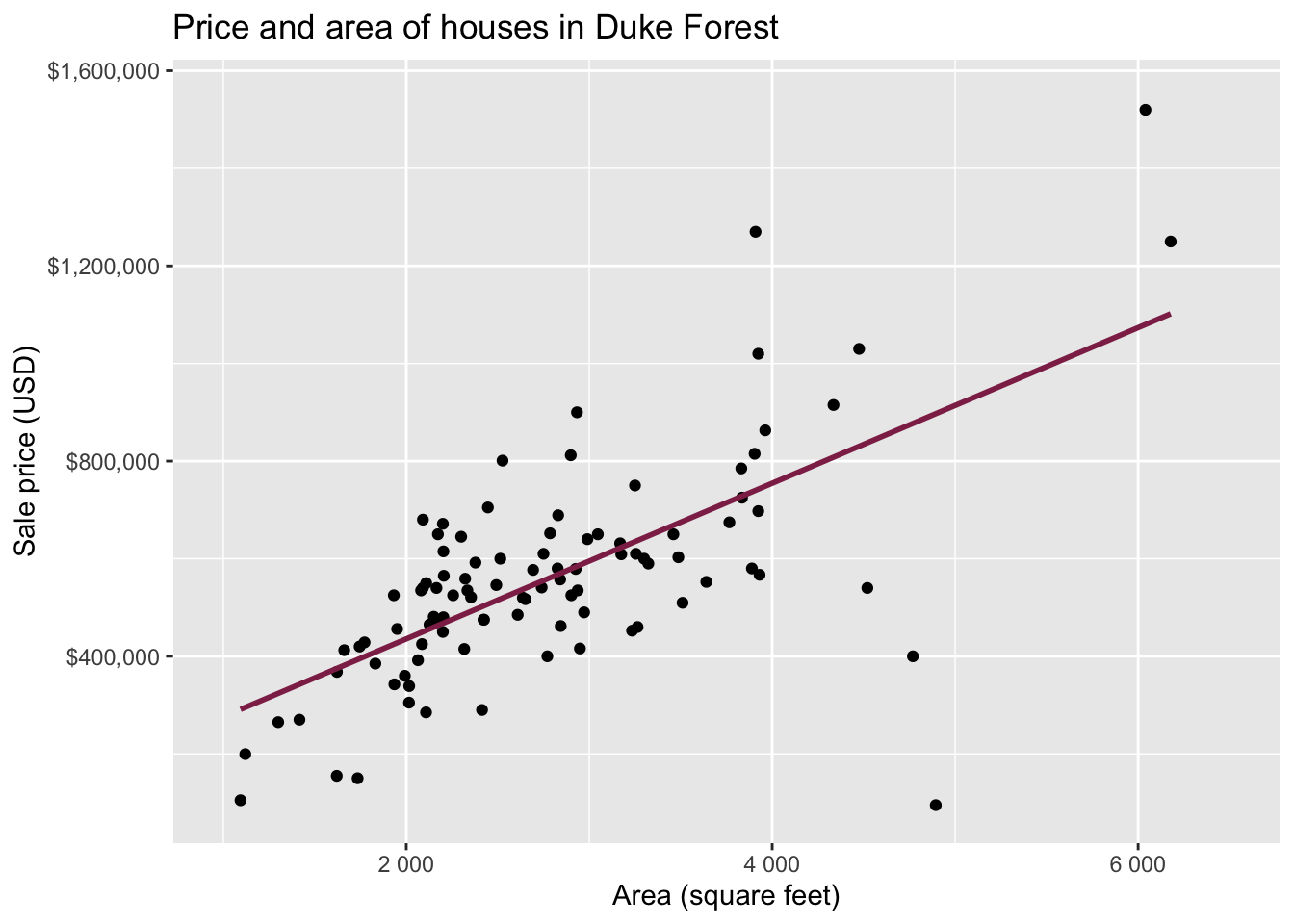

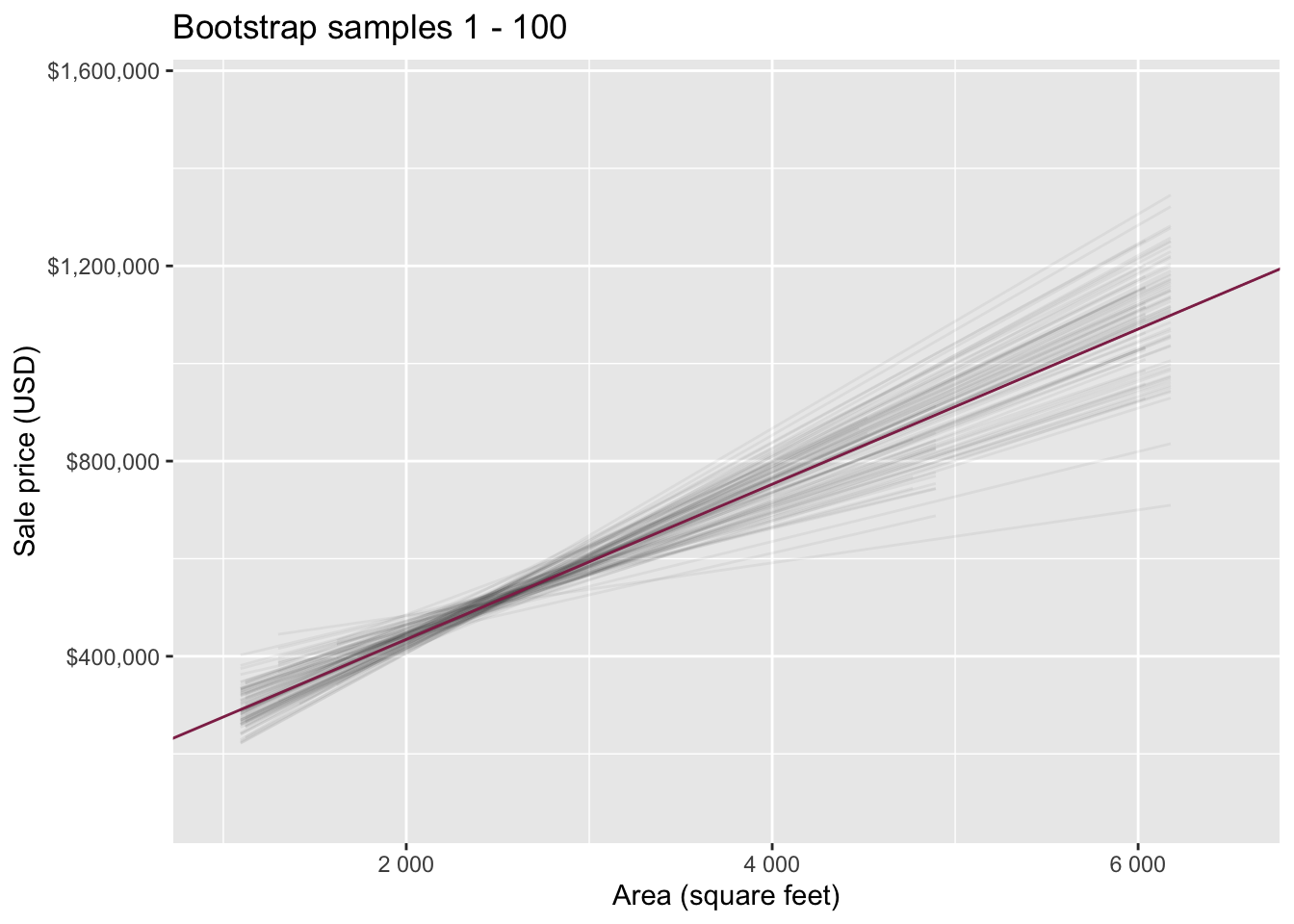

Data: Houses in Duke Forest

- Data on houses that were sold in the Duke Forest neighborhood of Durham, NC around November 2020

- Scraped from Zillow

- Source:

openintro::duke_forest

Goal: Use the area (in square feet) to understand variability in the price of houses in Duke Forest.

Exploratory data analysis

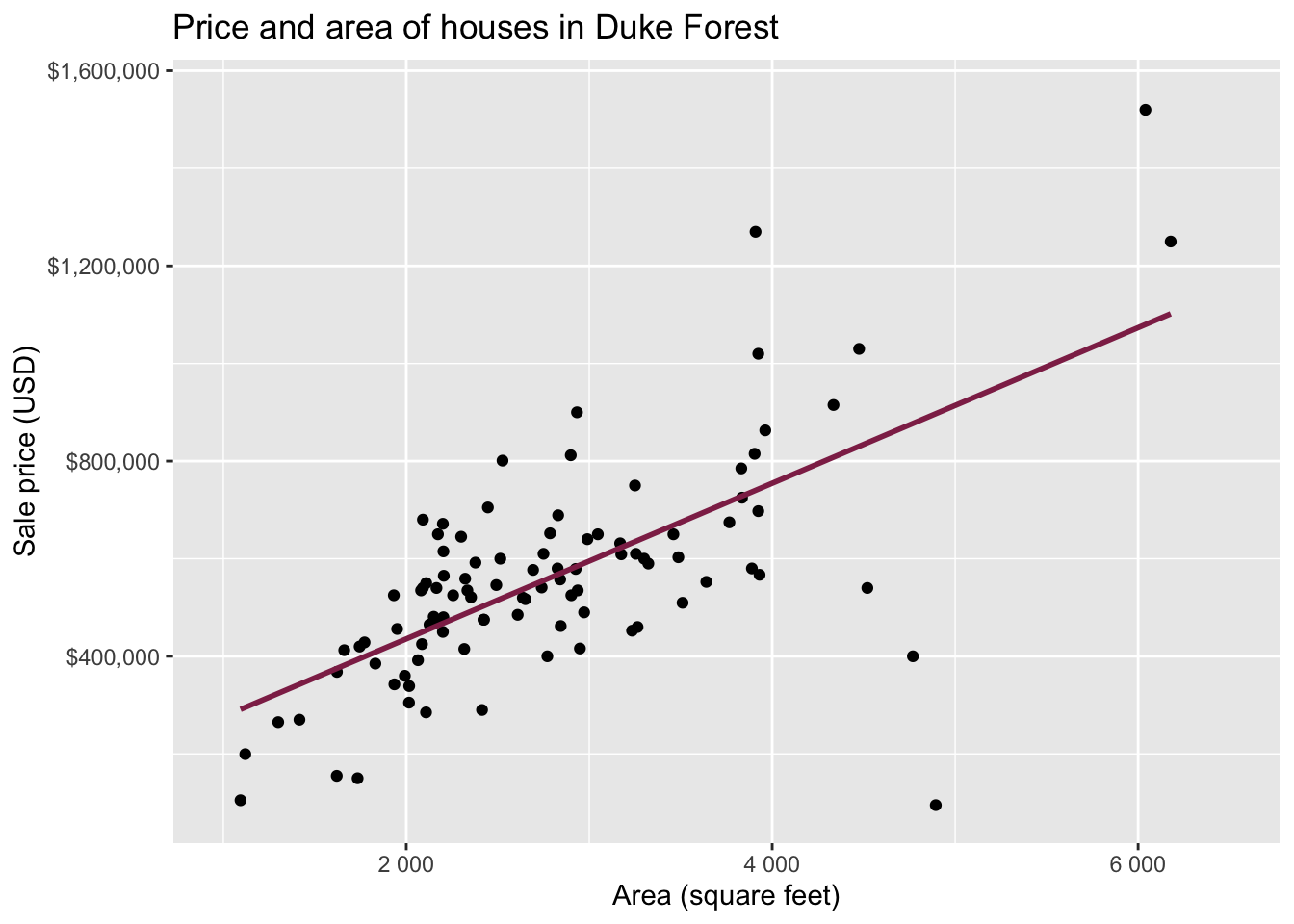

Statistical inference

Statistical inference provide methods and tools so we can use the single observed sample to make valid statements (inferences) about the population it comes from

For our inferences to be valid, the sample should be random and representative of the population we’re interested in

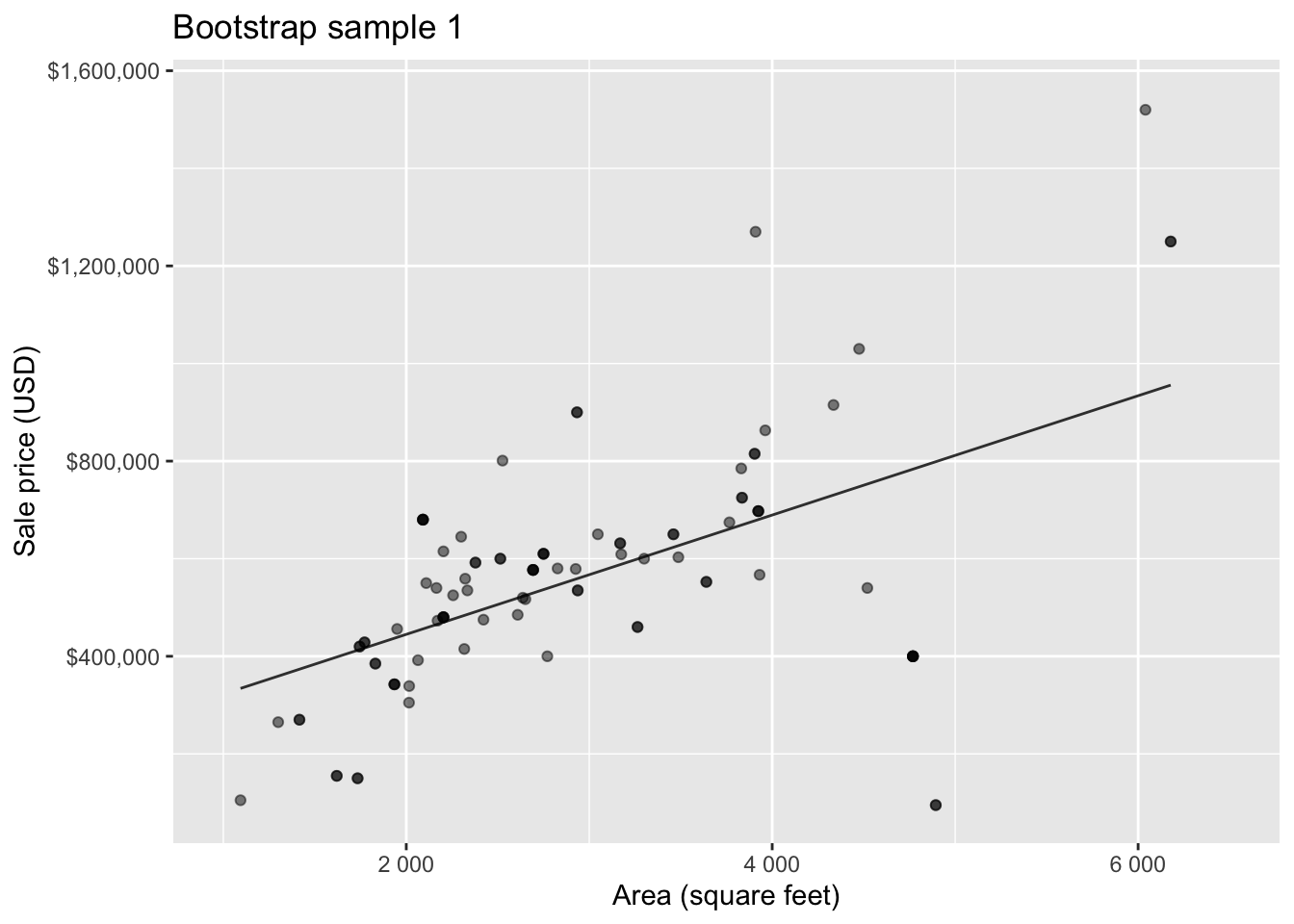

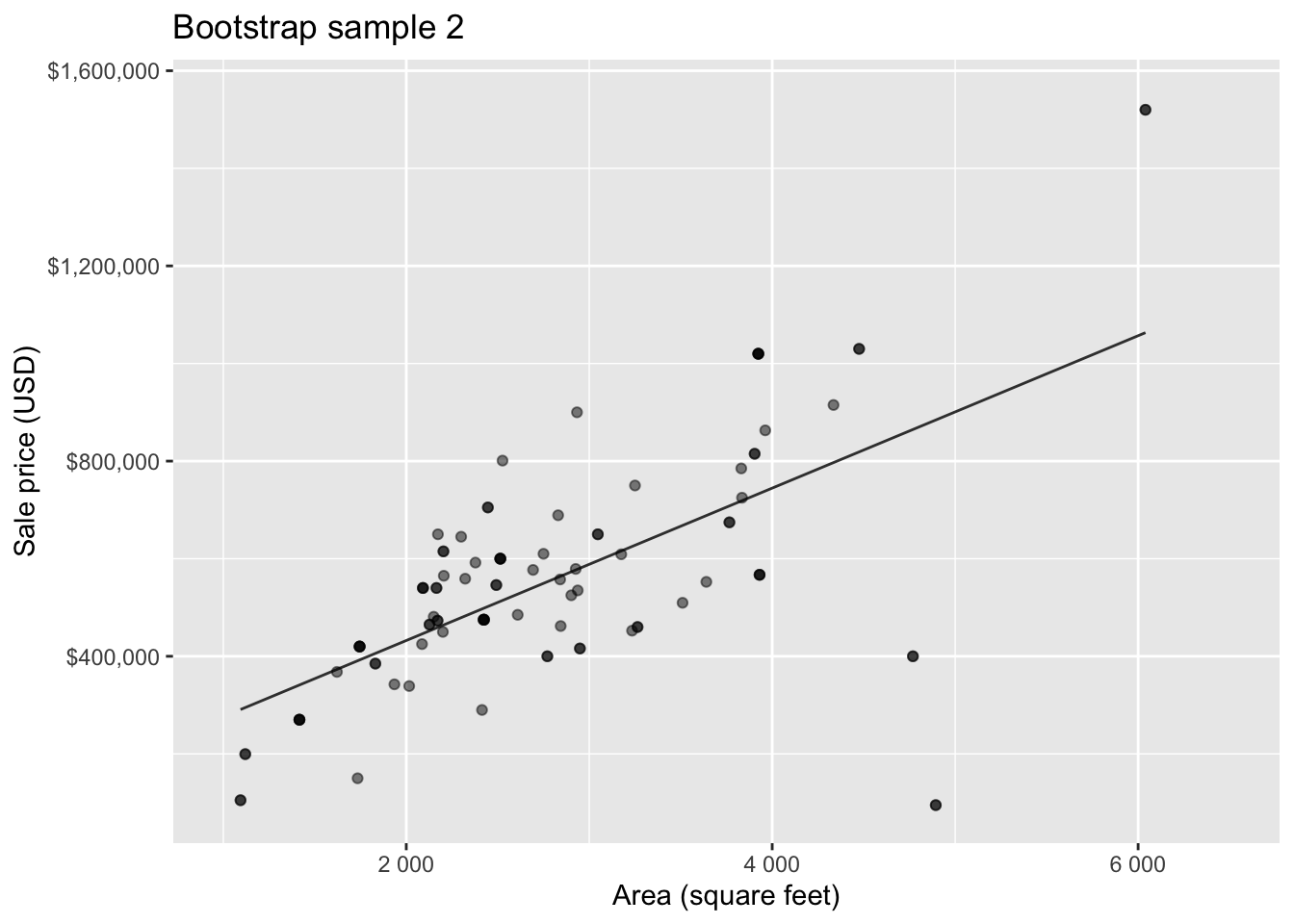

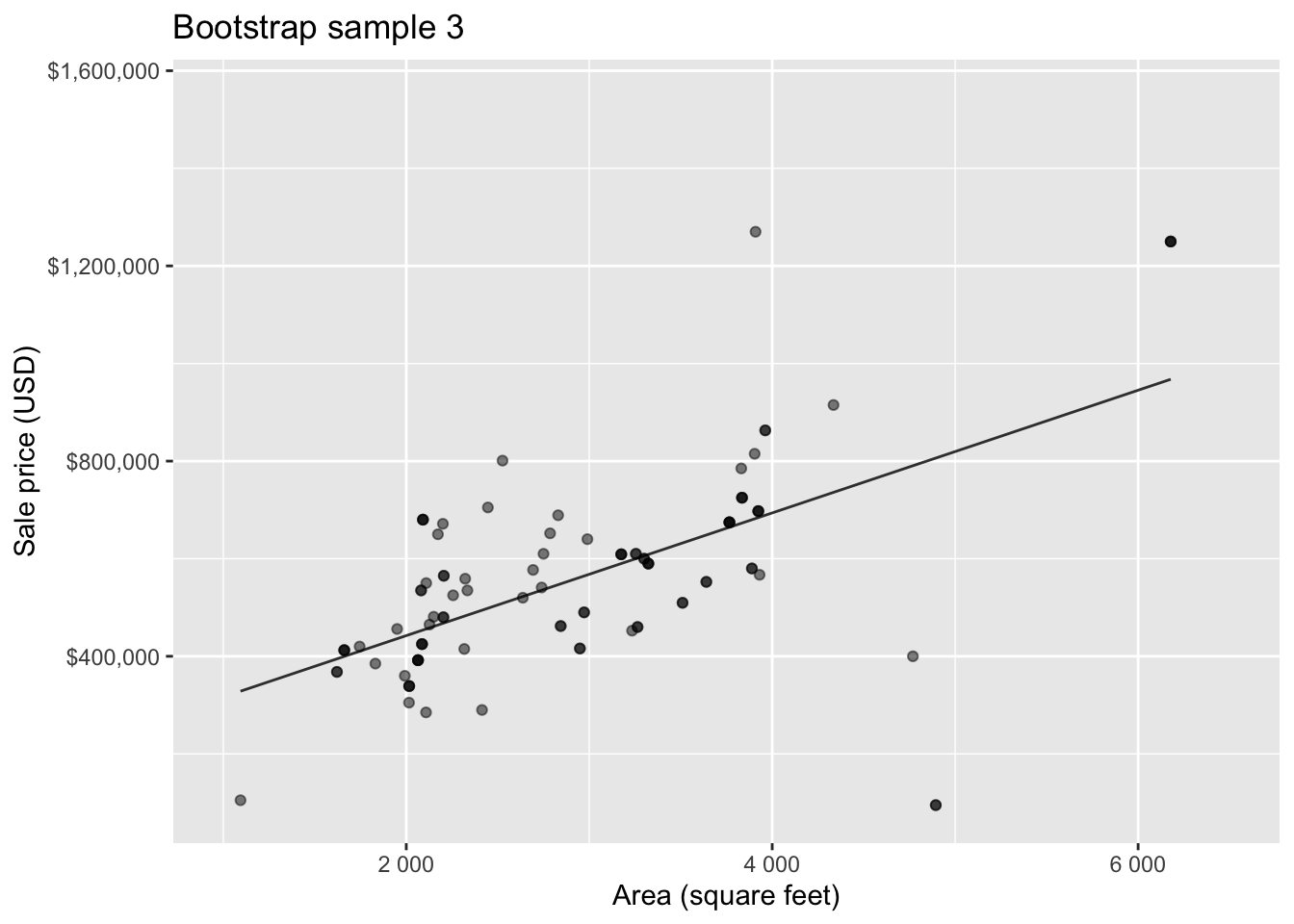

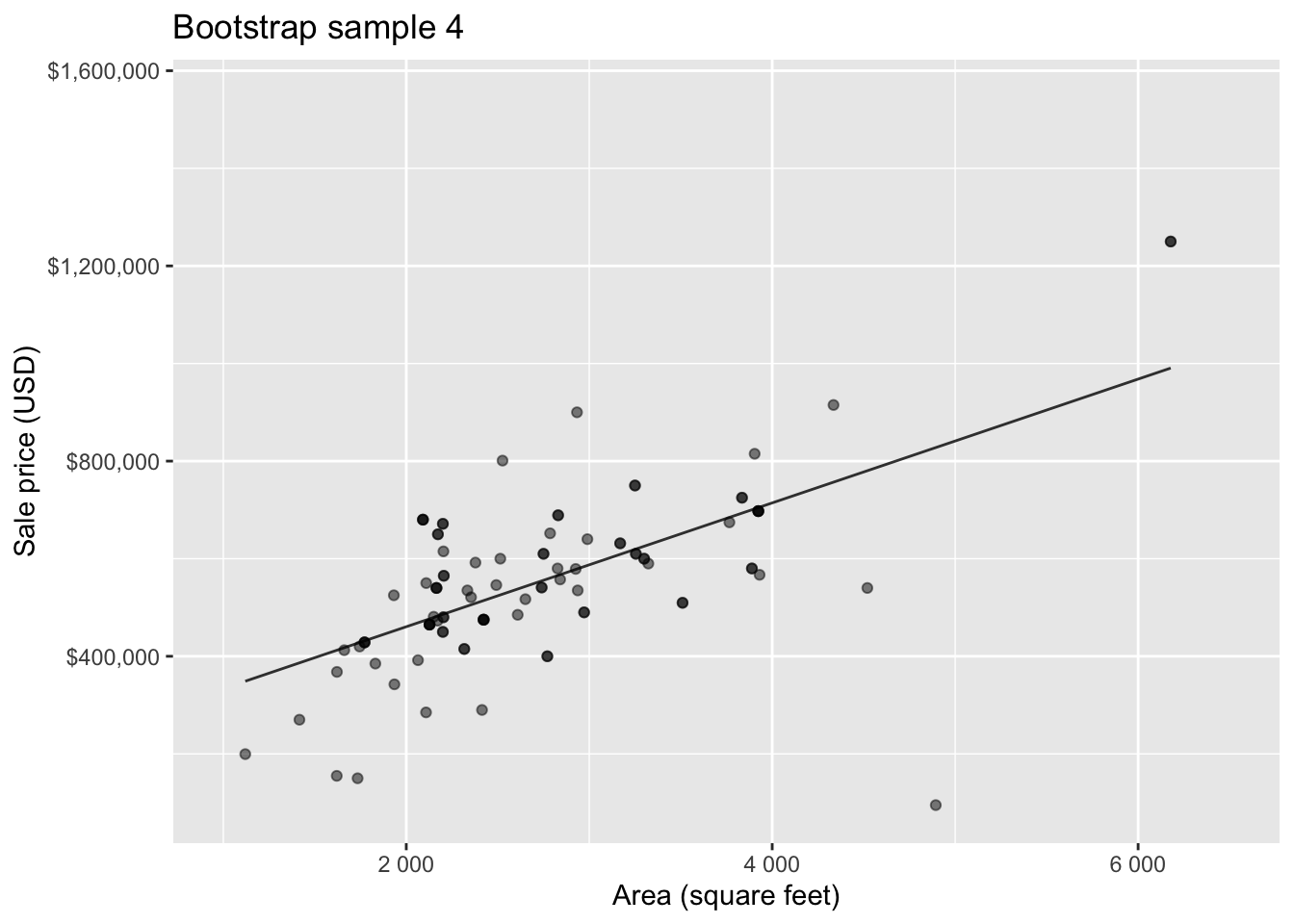

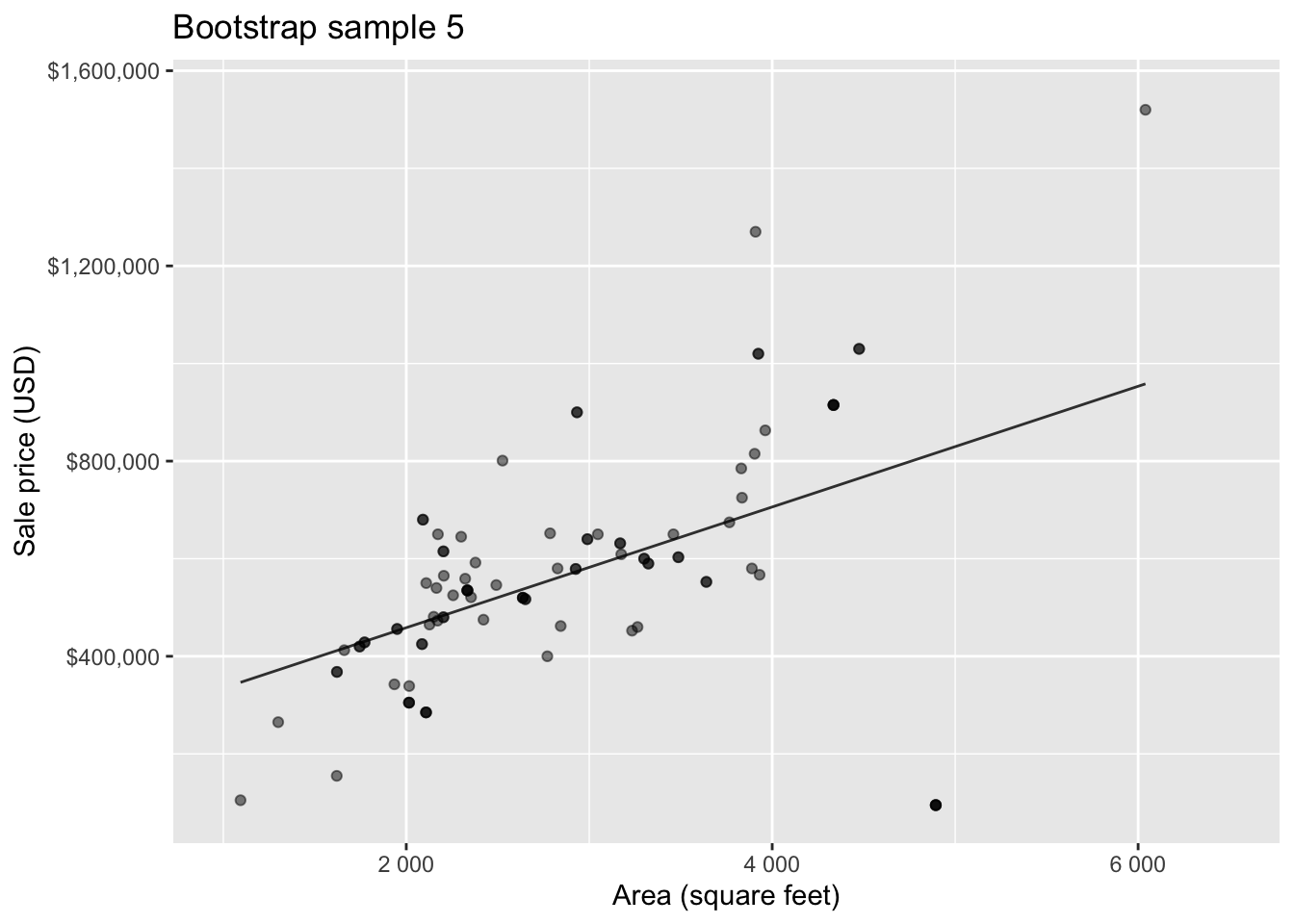

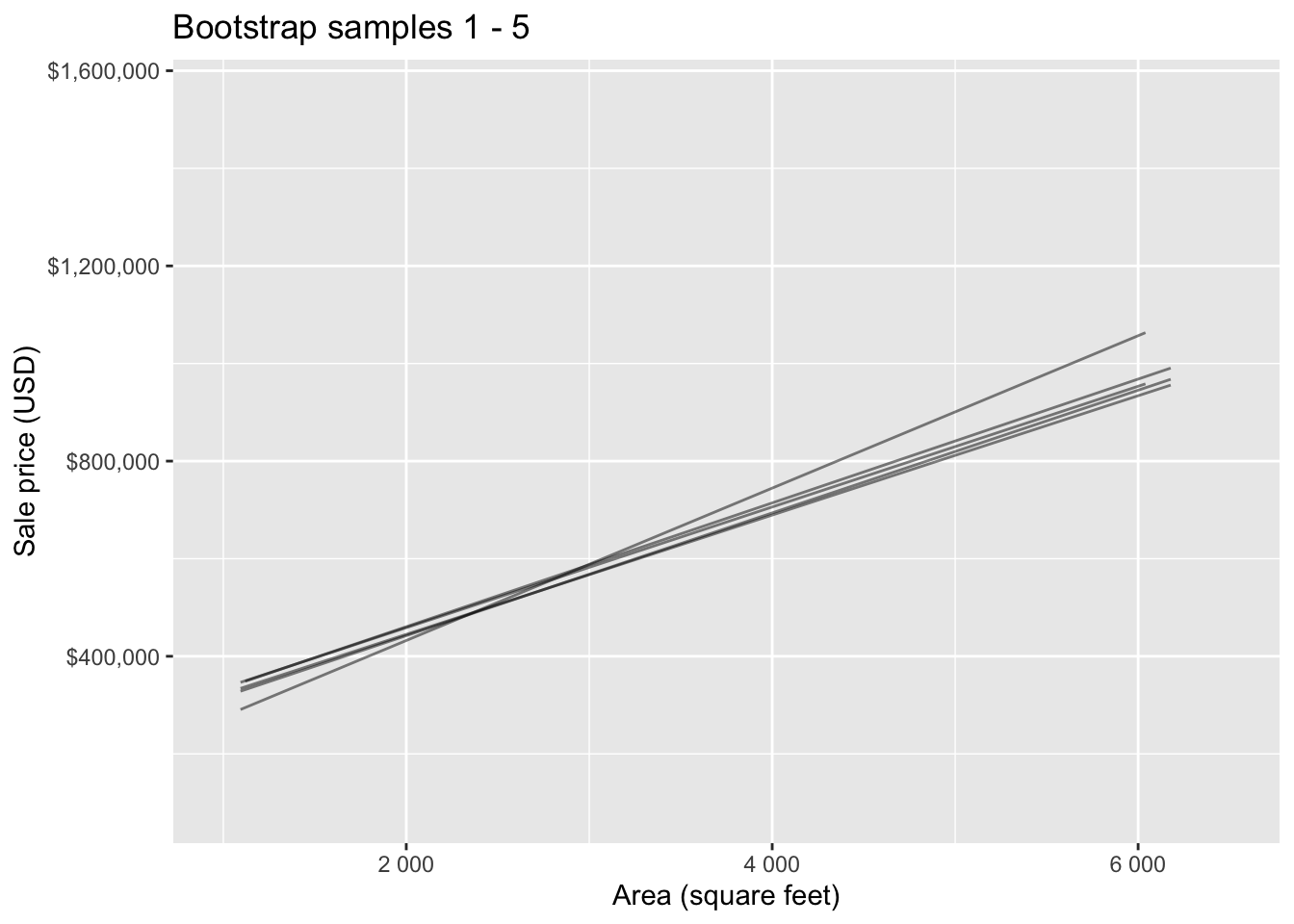

Bootstrap sample 1

Bootstrap sample 2

Bootstrap sample 3

Bootstrap sample 4

Bootstrap sample 5

so on and so forth…

Bootstrap samples 1 - 5

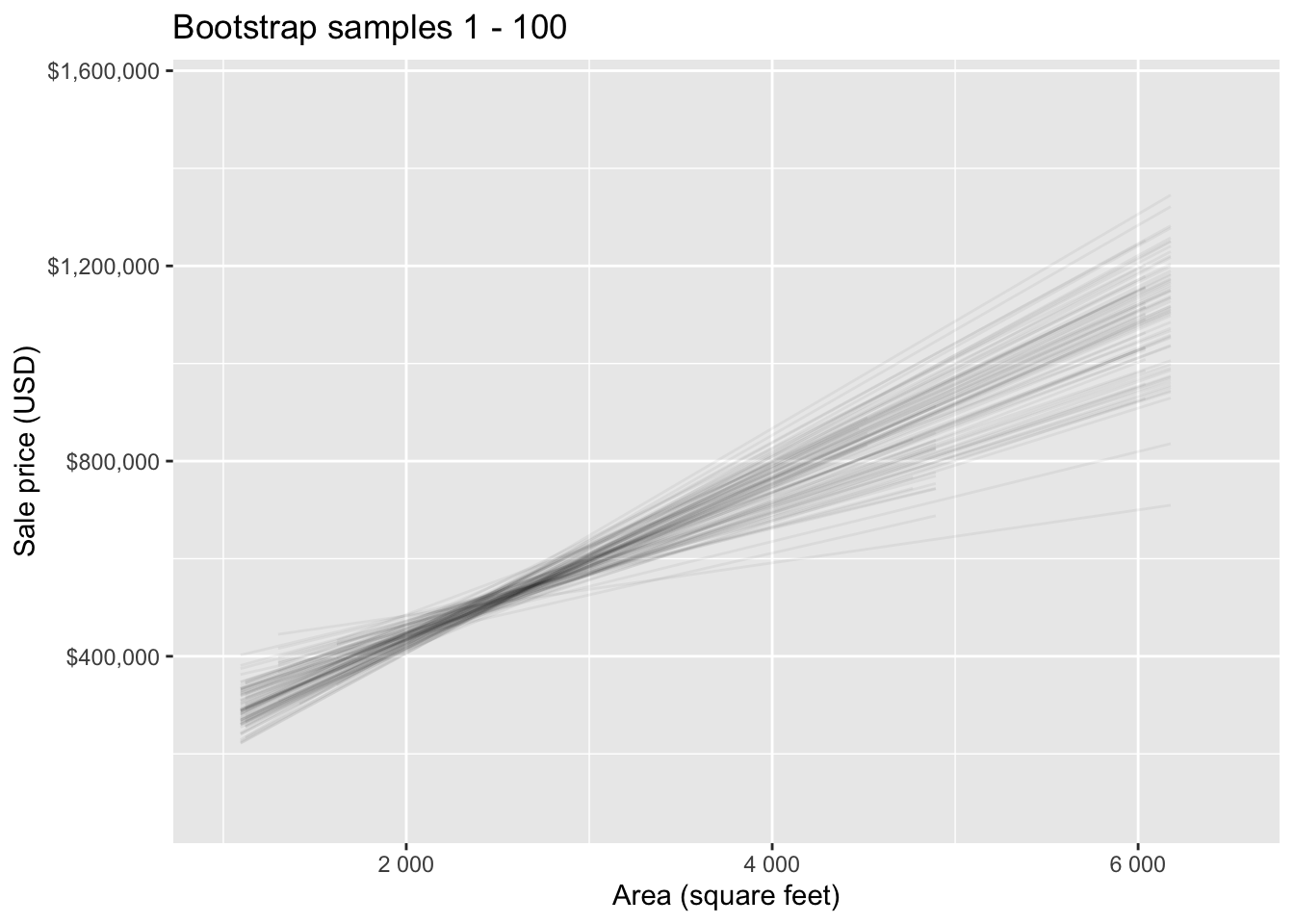

Bootstrap samples 1 - 100

Slopes of bootstrap samples

Fill in the blank: For each additional square foot, the model predicts the sale price of Duke Forest houses to be higher, on average, by $159, plus or minus ___ dollars.

Slopes of bootstrap samples

Fill in the blank: For each additional square foot, we expect the sale price of Duke Forest houses to be higher, on average, by $159, plus or minus ___ dollars.

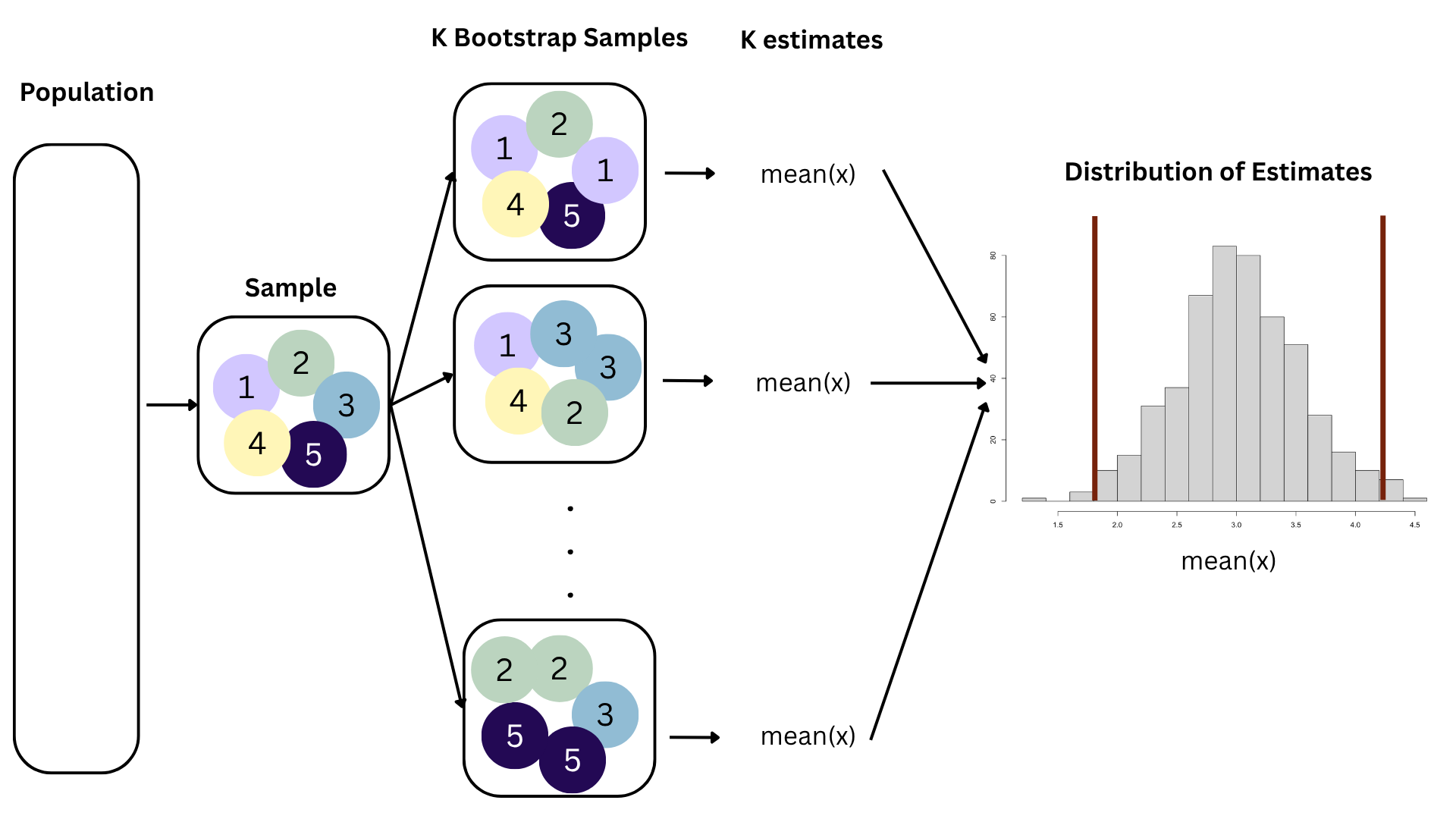

Confidence level

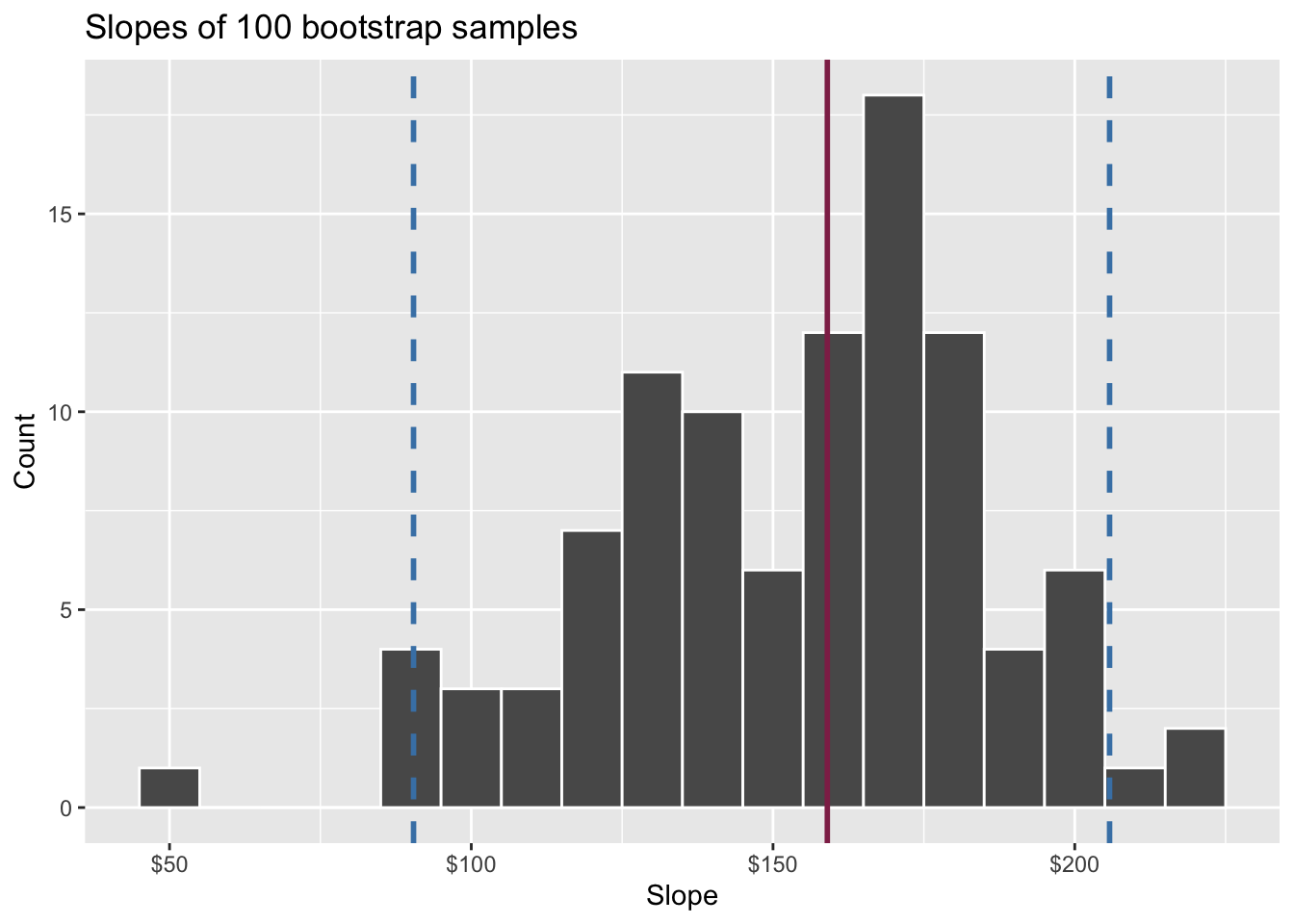

How confident are you that the true slope is between $0 and $250? How about $150 and $170? How about $90 and $210?

95% confidence interval

- A 95% confidence interval is bounded by the middle 95% of the bootstrap distribution

- We are 95% confident that for each additional square foot, the model predicts the sale price of Duke Forest houses to be higher, on average, by $90.43 to $205.77.

Precision vs. accuracy

If we want to be very certain that we capture the population parameter, should we use a wider or a narrower interval? What drawbacks are associated with using a wider interval?